Abstract

This article systematically studies four typical RWA projects in the United States: Real Estate RWA (RealT), Fixed Income RWA (Ondo Finance), Supply Chain Finance RWA (Centrifuge), and Pre-IPO Equity RWA. The research aims to reveal the institutional logic and technical underlying of RWA in the global financial reconstruction wave in 2025 through case disassembly, regulatory structure analysis, and return model comparison.

1. Asset Structure Level: RealT breaks through the threshold for real estate investors through an SPV confirmation and Reg D/S compliant issuance model, achieving small fractional investments; Ondo, with U.S. treasury bonds as the underlying asset, utilizes the custody mechanism of BlackRock and Coinbase to achieve on-chain money market fund functionality; Centrifuge uses the Tinlake mechanism to put supply chain receivables on-chain, with MakerDAO providing collateral DAI liquidity, forming a new paradigm for on-chain factoring.

2. Regulatory Supervision Level: The study finds that the main regulatory paths for RWA structural design by the U.S. SEC are Reg D, Reg S, Reg CF, and Reg A+, with core principles focusing on investor qualifications, information disclosure obligations, and liquidity constraints.

3. Technical Support Level: Technically, the Aave module provides fund bridges for institutions and ensures the effectiveness of fund flows, while Chainlink oracles guarantee the reliability of asset valuations, collateral rates, and income settlements.

4. Risks and Outlook: Future RWA development will be restricted by three key bottlenecks: compliance disclosure costs, cross-border custody compliance, and stablecoin anchoring risks. However, from the trend of institutional participation and return-risk matching perspectives, RWA is viewed as one of the most sustainable asset classes in on-chain finance.

Keywords: RWA, Tokenization, Digital Securities, Asset On-Chain, Supply Chain Finance

01 Real Estate RWA (RealT): Asset Confirmation, Fractional Participation, and Breaking Investor Thresholds

1.1 Development Logic of U.S. Real Estate RWA

Real estate is one of the earliest asset classes to be tokenized and is also the segment in RWA that integrates most with the real financial system. Its core logic lies in: through on-chain confirmation, fractional governance, and smart contract allocation mechanisms, the high thresholds and low liquidity structures of traditional real estate are completely reshaped. RealT, as the most representative practical platform in the U.S., has built a compliant tokenized real estate system based on Ethereum and Gnosis chains since 2019, becoming a model for asset on-chain and regulatory integration.

Compared to traditional REITs (Real Estate Investment Trusts), the innovation of RealT's model includes:

1) SPV (Special Purpose Vehicle) token issuance structures based on specific properties, enabling independent governance for each property;

2) Rent distribution based on stablecoins (USDC/DAI), which enhances traceability and immediacy of returns;

3) After KYC/AML certification, investors can participate in overseas property income distribution with an extremely low financial threshold (usually starting at $50).

1.2 Asset Confirmation and SPV Structure Design

In the RealT system, the confirmation process is the most critical regulatory step. Every property must complete property rights review, valuation certification, and SPV registration before being put on-chain. This SPV is typically established in Michigan or Delaware, existing in the form of an LLC (Limited Liability Company), with RealT responsible for property management and income distribution. The table below presents the standardized asset confirmation process of RealT.

Note: RealT adopts a dual-layer structure of SPV + Token, which does not fundamentally avoid the classification of Token as securities; on the contrary, RealT's Tokens are explicitly viewed as securities, opting to issue them through Reg D / Reg S exemption paths, thus not requiring public registration (Non-Public Offering).

1.3 Fractional Participation and Breaking Investor Thresholds

The success of RealT lies in lowering thresholds and enhancing participation. Traditional real estate investments often require millions of dollars, while RealT achieves fractional participation through tokenization. Investors can freely choose to invest in individual properties, with returns automatically distributed according to Token proportions.

Note: The circulation of RealT's tokens primarily relies on its self-built Marketplace, and in some cases, integrates with DEXs like Uniswap. Its advantage lies in instant liquidity and global participation, but due to regulatory thresholds, its investor group still focuses on accredited investors with KYC certification.

1.4 Economic Benefit Model and On-Chain Income Distribution

The income of the RealT platform mainly comes from rent distribution and secondary market price differences.[4] Based on public data (2025), RealT properties have an average net rental yield of 10%, maintaining high returns even after deducting property management and maintenance costs.

Note: The value of RealT lies not only in cash flow stability but also in transforming real estate into quasi-monetized assets. In the high interest rate period of the Federal Reserve, its stable yield and asset preservation characteristics make it a secure yield source for stablecoin ecosystems like USDC, with some DeFi protocols already incorporating RealT tokens as collateral assets.

1.5 Regulatory Challenges and Future Outlook

The advantages of the RealT model come with risks: first, the regulatory gray area issue. Although the project follows the Reg D/Reg S framework, whether its token secondary market trading constitutes the circulation of unregistered securities remains a legal dispute. Second, the compliance expansion bottleneck, where different states have legal differences regarding property transactions and SPV establishment, complicating asset standardization. Third, the oracle and on-chain valuation issues, with RealT currently adopting a fixed valuation method and lacking a dynamic market pricing mechanism.

However, from a macro trend perspective, real estate RWA is gradually integrating with traditional financial systems. Institutions like BlackRock and Franklin Templeton are exploring structured combinations of on-chain funds + physical assets; meanwhile, the open regulatory environment in markets like Hong Kong and the UAE provides policy soil for the international replication of the RealT model.

1.6 Case Studies

1.6.1 Detroit Rental Residential Project (2024)

Detroit is a key city for RealT's layout, with its low housing prices and stable rentals making it an ideal target for high returns and low volatility. Taking a residential project that will be on-chain in 2024 as an example[5]:

- Property Value: USD 72,500

- Token Issuance: 1,450 tokens (each at $50)

- Annual Net Rental Income: USD 7,400

- Investor Return Rate: 10.2%

- Payment Method: USDC automatically distributed weekly

- Investor Source: Mainly KYC investors from the EU, Canada, and Singapore

Success Point: The success of this project lies in the combination of real-world assets and on-chain contracts. Rental income is distributed in real-time through stablecoins, and investors can directly verify income receipts through blockchain explorers; property management data and lease contracts are uploaded in hash form for immutable audit.

Risk Point: Operations (property management, taxes, tenant disputes) remain off-chain decision factors; tokenization cannot replace on-site management. Feedback suggesting weak operational integration has emerged in RealT's expansion, indicating that on-site KPIs and on-chain disclosures should become normalized. During due diligence, it is crucial to obtain on-site due diligence reports, custody/insurance terms, and property management contracts.

1.6.2 St. Regis Aspen or Aspen Coin

In 2018, Elevated Returns tokenized part of the equity of the St. Regis Aspen resort in Colorado (Aspen Coin),[6] issuing it in the form of security tokens to accredited investors and raising approximately $18 million. This case is often seen as a representative model of legal first, then technical.

- Property Value: Raised about $18 million, representing about 18% equity in the hotel, allowing an estimated overall valuation of the hotel at around $95 million - $100 million+[6].

- Token Issuance: Priced at $1/coin during issuance, leading to the issuance of 18,000,000 Aspen Coins.

- Annual Net Rental Income: This product pays dividends based on hotel profits; the annual return depends on the hotel's operational data, publicly disclosed as dividends to shareholders.

- Investor Return Rate: As an equity product, returns come from hotel operating profits and capital gains; the project does not promise fixed returns.

- Payment Method: Publicly available for purchase in USD, BTC, ETH, etc.; dividend and interest distributions are conducted through traditional payment or custodial processes under legal and custodial frameworks, with on-chain tokens serving registration and circulation purposes.

- Investor Source: Mainly accredited, institutional, and restricted investors, with a minimum purchase limit set (10,000 Tokens), targeting compliant investors[7].

Success Point: Prioritize solving legal and custody issues (SPV, trustees, securities registration), treating tokens as electronic securities, providing a compliant path for institutions and accredited investors, reducing regulatory friction.

Risk Point: High compliance costs and limited liquidity in the secondary market; suitable for high-value, low-frequency trading assets. For issues directed at institutions or family offices, compliance priority is often more important.

1.6.3 Roofstock onChain (Single Property NFT or LLC Structure)

Roofstock onChain puts single properties (often rental market houses) on-chain by establishing a single-member LLC and minting NFTs representing the LLC equity, creating a closed loop for on-chain trading and off-chain property transfer coordination. The platform is also aided by on-chain financing connections and compliant KYC.

- Property Value: Public transaction examples include $175,000 ( 2022 South Carolina property, USDC transaction )

- Token Issuance: Roofstock On Chain typically uses a single NFT (ERC-721) to represent the entire property.

- Annual Net Rental Income: Taking a $175k–$180k property as an example, typical rental returns will fluctuate according to the market, generally around 4–8% net rental return[8].

- Investor Return Rate: If it’s the entire property buyer, returns come from net rent + capital appreciation; if fractional holders (in case of fractionalization), distributed according to shares.

- Payment Method: USDC (stablecoin) can be used for payments combined with on-chain loans (Teller or USDC Homes), and fiat paths are also supported (platform supports multi-channel settlement).

- Investor Source: Targeting ordinary investors + real estate investors + blockchain community; transaction parties are mostly home buyers or investors, and the platform usually cooperates with KYC or compliance processes.

Success Point: Standardizing the business process of property transfer (LLC and NFT), resolves the junction issue of on-chain transactions and traditional land registration, boosts transaction efficiency, and supports on-chain financing.

Risk Point: If original mortgages or liens have not been clearly resolved, or lenders disagree with on-chain transfers, legal effect may be impacted, needing pre-chain repayment or consent. It is essential to clear mortgages/priority rights or obtain written consent before going on-chain.

1.6.4 Harbor (Failed Case of Student Apartment Project)

In 2019, Harbor attempted to tokenize college student apartment projects (such as The Hub at Columbia) but was forced to cancel or restructure the corresponding tokenization plan due to conflicts with existing lender terms and mortgage/priority issues, becoming a teaching case of lessons learned in the tokenization implementation process.

- Property Value[9]: $20 million

- Token Issuance: Cancelled, with no final issuance number or actual token circulation data

- Annual Net Rental Income: Project not completed, with no publicly available actual allocation data

- Investor Return Rate: No issuance took place, no historical return data

- Payment Method: The plan was to tokenize into a REIT, expected to combine fiat or on-chain settlement; however, the plan was withdrawn before execution, with details not fully disclosed

- Investor Source: Originally planned to target accredited or institutional investors and platform users, but since no issuance was completed, there is no actual investor composition data.

Failure Summary: Before promoting real estate tokenization, it is necessary to first address and obtain consent from all existing creditors, restructure debts, or legally create a clear order of priority; otherwise, even the best technical solutions may be rejected due to creditor laws or priority guarantees.

02 Fixed Income RWA (Ondo Finance): Product Design, Risk Control, and Institutional Investor Participation Logic

2.1 Background and Industry Positioning

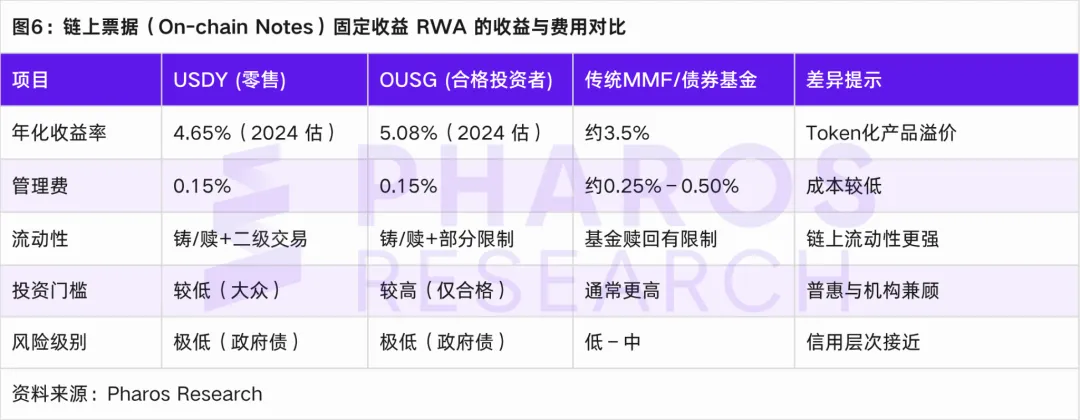

In the RWA (Real World Assets) sector, compared to real estate, private equity, or supply chain finance, fixed income assets, especially U.S. treasury bonds and short-term government securities, are regarded as a safe haven for on-chain funds due to their high credit rating and low yield volatility. Ondo Finance is a pioneer in this field, offering main products including USDY and OUSG, which correspond with broader investor entry and strict accredited investor channels. In June 2025, media reported that OUSG had achieved approximately $693 million scale on the ONDO platform, reflecting the scalability potential of fixed income RWA[1].

The core value of this model lies in: converting highly standardized, high credit-rated government bond assets off-chain into structured, tokenized forms through SPVs and smart contracts, thus linking to on-chain liquidity pools, achieving the three major benefits of enhanced liquidity, lowered investment thresholds, and compliant asset access.

2.2 Product Design Structure

2.2.1 Product Categories and Target Audience

- USDY: Targeting non-accredited investors and global users, backed by short-term U.S. treasury bonds and bank deposits, with floating annual yield type.

- OUSG: Targeting accredited investors (Qualified Purchasers) in the U.S., focusing on short-term U.S. government bonds, emphasizing high credit rating and low risk[10].

2.2.2 Structural Diagram

The following structure is chosen:

- Underlying Asset → U.S. Treasury Bonds or Short-Term Government Securities (e.g., T-Bills)

- Custody and Audit Agency (traditional assets management like BlackRock's BUIDL fund serves as the base)

- SPV/Trust Structure Set Up to Hold the Underlying Assets

- On-Chain Issue Token (USDY or OUSG) — Holders Own the Income Rights to the Underlying Assets But Have No Direct Ownership

- Smart Contract Configuration for Minting/Redeeming Mechanism + Income Distribution Mechanism (e.g., daily or weekly interest accrual)

- Secondary Market or Platform Market-Making Mechanism to Enhance Liquidity

2.2.3 Institutional Participation Logic

In the realm of fixed income RWA, the drive for institutional participation includes: first, traditional funds希望在链上保持配置但不愿放弃低风险收益; secondly, enabling asset managers to achieve a transparent, traceable, and low-friction issuance channel on-chain. For Ondo, its compliance background, custody arrangements, and collaboration with reputable asset management firms (such as BlackRock, Franklin Templeton) enhance its institutional credibility.[2] Moreover, tokenized government bonds can also serve as collateral assets within the DeFi ecosystem, improving fund efficiency.

2.3 Risk Control and Compliance Mechanism

In fixed income RWA products, the risk control and compliance mechanisms fundamentally form the core premise for acceptance by institutional investors. From current U.S. practices, these products typically use short-term U.S. government securities as the underlying asset to keep credit risk at a very low level, which is a key advantage distinguishing them from on-chain native assets. At the same time, income settlement mechanisms are automatically executed through smart contracts, significantly reducing human operation risks while enhancing transparency and auditability; the combination with custodial banks and third-party audit systems ensures a one-to-one correspondence between underlying assets and tokens, thereby establishing a dual guarantee of the real existence of assets and the credible mapping on-chain at the institutional level.

From the structural risk control perspective, its essence is not a single measure, but a dual-track system involving on-chain triggering mechanisms + traditional financial oversight. Specifically, regarding asset support rates, there are rigid constraints where the proportion of underlying assets to tokens must not be lower than 1:1, combined with a Proof-of-Reserve mechanism that allows for on-chain verifiability, supported by custodial banks providing audit endorsements; for liquidity management, it relies on 24/7 minting and redeeming mechanisms and market maker commitments and ensures full process traceability through on-chain event records; in terms of investor qualification control, it is achieved through an overlapping whitelist mechanism for KYC/AML and accredited investors system, linking on-chain permission management with U.S. securities regulatory requirements (e.g., SEC framework); the technical level relies on smart contract auditing, multi-signature governance, and audit reports on-chain to reduce protocol-level risks; additionally, in collateral and liquidity usage scenarios, all collateral actions are tracked and disclosed on-chain, avoiding the buildup of hidden leverage risks.

From a compliance pathway perspective, the issuance of such tokens generally relies on the Reg D and Reg S frameworks under U.S. securities laws, using private placement exemptions to avoid public issuance registration requirements while strictly limiting the range of investors and information disclosure obligations; the custody of underlying assets must conform to banking regulatory systems and ensure asset authenticity and independence through regular audits; in the design of trading and exit mechanisms, on-chain transfers are not completely free but incorporate investor eligibility checks and compliance restrictions, thus achieving a dynamic balance between liquidity and regulation.

Overall, the essence of the current RWA risk control system is transforming traditional financial intermediaries and audit trust mechanisms into verifiable and automatically executed combinations on-chain. This model does not diminish regulation but rather strengthens regulatory execution on the technical level. However, it is essential to note that risks have not vanished; they have shifted from being primarily credit risks to structural risks and compliance execution risks, such as custodian failures, discrepancies between on-chain data and real assets, or uncertainties due to regulatory policy changes. Therefore, the question of whether RWA can achieve large-scale institutional implementation in the future hinges not on technological maturity but on the long-term stability and regulatory compliance of this on-chain + off-chain integrated risk control system.

2.4 Income Model and Quantitative Analysis

Within fixed income RWA systems, the core logic of the income model has not departed from traditional finance, but instead achieves more efficient income redistribution and enhanced liquidity in the on-chain structure. Ondo Finance's treasury RWA products primarily derive income from interest on the underlying U.S. treasury bonds, combined with structural premiums provided by the operational efficiency of the fund pool and liquidity premiums granted by the on-chain secondary market. According to actual data, the annualized yield of the USDY and OUSG products in 2024 is about 4.6%–5.4%[3], a level that is not only significantly higher than most traditional money market funds in the current interest rate environment but also reflects the advantages of on-chain assets in terms of cost compression and distribution efficiency. More importantly, these products, through tokenization, repackage income-generating assets that were originally confined within institutional systems, allowing them to simultaneously target both retail and accredited investor groups, further creating market expansion value beyond the income structure.

From a cost and structural perspective, on-chain notes exhibit clearer lightweight characteristics compared to traditional MMFs (money market funds) or bond funds. On one hand, management fees have significantly decreased, reflecting a compression of intermediaries; on the other hand, the on-chain minting–redeeming–trading mechanism significantly enhances capital turnover efficiency, allowing investors to achieve liquidity release through the secondary market without relying solely on fund redemption windows. This near-real-time liquidity essentially represents a structural transformation of traditional assets through DeFi mechanisms; its significance lies not only in the improvement of yields but also in the enhancement of capital utilization efficiency and asset combinability. In other words, the competitiveness of RWA is shifting from higher yields to greater efficiency under equivalent risks.

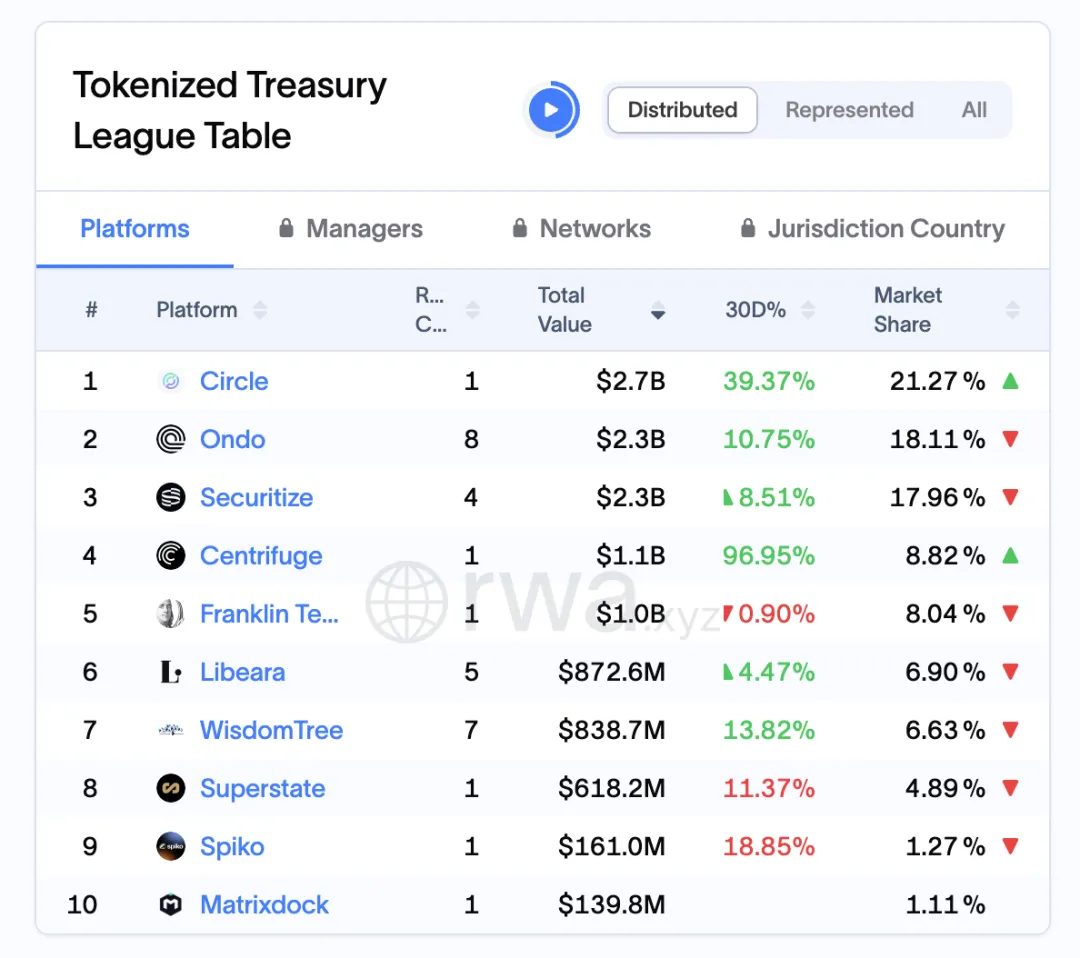

According to data from the RWA.xyz platform, as of April 1, 2026, Ondo has locked $2.3 billion in assets in the U.S. treasury RWA market, holding approximately 18.11% market share, becoming one of the leaders in this segment.

Figure 7: Global Top 10 RWA Issuance Protocol Market Cap and Market Share (as of April 1, 2026)

Data Source: rwa.xyz/treasuries, Pharos Research

2.5 Institutional Participation and Secondary Mechanisms

As the fixed income RWA system gradually matures, the participation pathways of institutional investors and the construction of secondary market mechanisms become key variables determining product scale and liquidity. From Ondo Finance's practice, its core strategy is not merely to bring in institutional capital but to effectively connect traditional asset management institutions (like asset managers and custodial banks) with on-chain investors through a structural design that expresses off-chain asset management and on-chain liquidity. In this process, institutions take on more responsibilities for selecting underlying assets, portfolio management, and compliance custody, while the on-chain portion handles fractionalization, liquidity release, and investor distribution, forming a new cooperative relationship that decouples functions but links risks. This structure enables RWA products to meet institutional demands for safety and compliance while accommodating the need for flexibility and tradability among on-chain users.

Furthermore, the secondary market mechanism is the core driving force behind the transition of RWA from fund-like products to tradable asset categories. Secondary trading mechanisms activate token circulation and enhance asset fundraising effectiveness. Ondo’s Nexus platform claims it can achieve an on-demand mint and redeem mechanism, enhancing liquidity[2]. This mechanism fundamentally reshapes the traditional fund issuance-driving liquidity model, allowing investors to no longer rely entirely on issuers to provide liquidity outlets but to realize share transfers through matchmaking trades on-chain, significantly shortening capital exit cycles. At the same time, the introduction of market-making mechanisms and liquidity pools has also somewhat reduced price volatility's liquidity discount issues, allowing RWA assets to gradually exhibit trading characteristics similar to bond ETFs.

At a deeper level, there is a clear positive feedback loop between institutional participation and secondary mechanisms: the entry of institutions improves the quality and stability of underlying assets, thereby enhancing market confidence; more efficient secondary liquidity, in turn, boosts institutional allocation willingness and fund turnover efficiency. Once this cycle is established, it will propel the RWA market into a phase of scaled growth. However, it is important to note that this model still relies on strict compliance boundaries and investor access mechanisms; particularly under the U.S. regulatory framework, secondary trading is often restricted by transfer limitations and accredited investor rules, which somewhat constrains the achievement of completely free circulation.

The current secondary mechanism created by Ondo essentially attempts to build an on-chain fixed income market infrastructure; its significance lies not only in enhancing the liquidity of individual products but also in providing a unified trading and pricing framework for various RWA assets in the future. If this mechanism can continue to evolve and gradually incorporate more market makers, structured products, and interest rate derivatives, then the RWA market could potentially evolve from a passive income asset pool to a complete yield curve and risk-layered on-chain bond market. At that point, institutional participation will no longer be an incremental variable but will become a core component of market operation.

2.6 Challenges, Trends, and Implications for the Hong Kong Market

From a broader perspective, while the pioneering exploration of the RWA track in the United States has verified feasible paths for asset on-chaining, its development still faces multiple structural constraints, including ununified regulatory frameworks, complex legal ownership connections between on-chain and off-chain, liquidity dependence on a few platforms, and uneven transparency of underlying assets. Meanwhile, the market is gradually forming clear trends: first, asset types are extending from standardized assets like short-term treasury bonds to more complex categories such as credit and private equity fund shares; secondly, compliance infrastructure (like KYC/AML, custody, auditing) is continuously strengthening; thirdly, leading institutions are accelerating entry to drive scaled development. In this context, if China and Hong Kong markets wish to seize RWA development opportunities, they can leverage their respective advantages in institutional supply and scene implementation, such as China strengthening blockchain and traditional finance connections to explore RWA pathways more suitable for the local market. Hong Kong, as an international financial center, can leverage its mature financial market and global investor base to promote compliant cross-border circulation of RWA, providing an important bridge for the expansion of the global RWA market. Especially regarding RWA's cross-border liquidity and international investor access, Hong Kong is poised to become an important experimental field and development force for this emerging asset category.

Overall, while the U.S. has achieved a leading position in RWA development, its future large-scale growth still faces significant challenges in compliance and liquidity. The openness and innovative capability of China and Hong Kong markets may provide new opportunities and perspectives for the further expansion of the global RWA market.

06 References

[1] Coindesk: Ondo Finance Debuts $693M Treasury Token on XRP Ledger Amid Soaring RWA Trend

[2] Ondo.finance: Introducing Ondo Nexus Delivering Instant Liquidity for Third-Party Tokenized Treasuries, Leveraging Assets from BlackRock, Franklin Templeton, Wellington Management, and WisdomTree

[3] Plume.org: Plume Network Taps Ondo Finance to Broaden RWAfi Ecosystem with Tokenized US Treasuries

[4] outliermedia.org: The real estate scheme gobbling up Detroit, one digital token at a time

https://outliermedia.org/crypto-real-estate-realt-cryptocurrency-detroit/

[5] RealT White Paper - https://realt.co/wp-content/uploads/2019/05/RealToken_White_Paper_US_v03.pdf

[6] Aspentime - https://www.aspentimes.com/trending/in-18-million-deal-nearly-one-fifth-of-st-regis-aspen-sells-through-digital-tokens

[7] Pwco - https://www.pwco.com.sg/insights/blockchain-real-estate-part-iii/

[8] Nftnow - https://nftnow.com/news/roofstock-onchain-origin-story-sell-third-property-via-nft-marketplace/

[9] Harbor Cancels Tokenized REIT of University Dorm 'The Hub at Columbia' -

https://tokenist.com/harbor-cancels-tokenized-reit-of-university-dorm-the-hub-at-columbia/

[10] RWA.xyz: https://app.rwa.xyz/assets/OUSG

[11] Gov.centrifuge: https://gov.centrifuge.io/t/cp95-pop-new-silver-ns3/5603

[12] Gov.centrifuge: https://gov.centrifuge.io/t/issuer-harbor-trade-credit/141

[13] U.S. Securities and Exchange Commission: https://www.sec.gov/resources-small-businesses/regulation-crowdfunding-guidance-issuers

[14] State of the Pre-IPO Market -

https://www.hiive.com/market-reports/state-of-the-pre-ipo-market-2026-annual-report

[15] https://www.blueowlcapitalcorporation.com/investors/sec-filings

[16] https://app.rwa.xyz/credit

[17] https://dune.com/discover/content/trending

Disclaimer: This article represents only the personal views of the author and does not represent the position and views of this platform. This article is for information sharing only and does not constitute any investment advice to anyone. Any disputes between users and authors are unrelated to this platform. If the articles or images on the webpage involve infringement, please provide relevant proof of rights and identity documents and send an email to support@aicoin.com. The relevant staff of this platform will conduct an investigation.