Author: Ba Jiuling, Wu Xiaobo Channel

The AI bull market that has rebounded for a month and a half seems to be coming to an end.

From last Friday to yesterday, global capital markets faced a wave of selling frenzy.

Last Friday was the worst, as global stock markets plunged widely, with the South Korean Composite Index dropping 6.12%, temporarily reaching the circuit breaker limit. The Nikkei 225 Index plummeted by 6.22%, and the three major U.S. stock indexes performed poorly, with the Nasdaq index falling 1.54%, and the Shanghai Composite Index losing 2.5% over two days, shaking investor confidence.

By this Monday, the A-shares and Hong Kong stock markets continued to maintain weakness, with the Nikkei 225 Index decreasing by 0.97%. After the U.S. stock market opened at night, the three major indexes also showed weakness.

Who has pulled the bull back from the market?

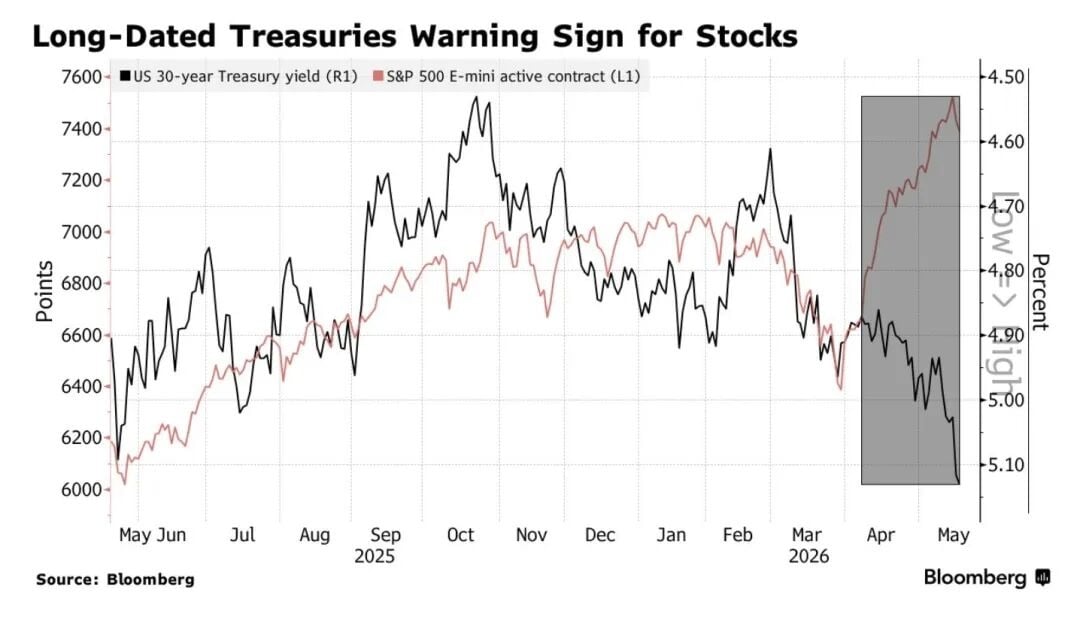

According to Morgan Stanley, the main suspect is the bond market.

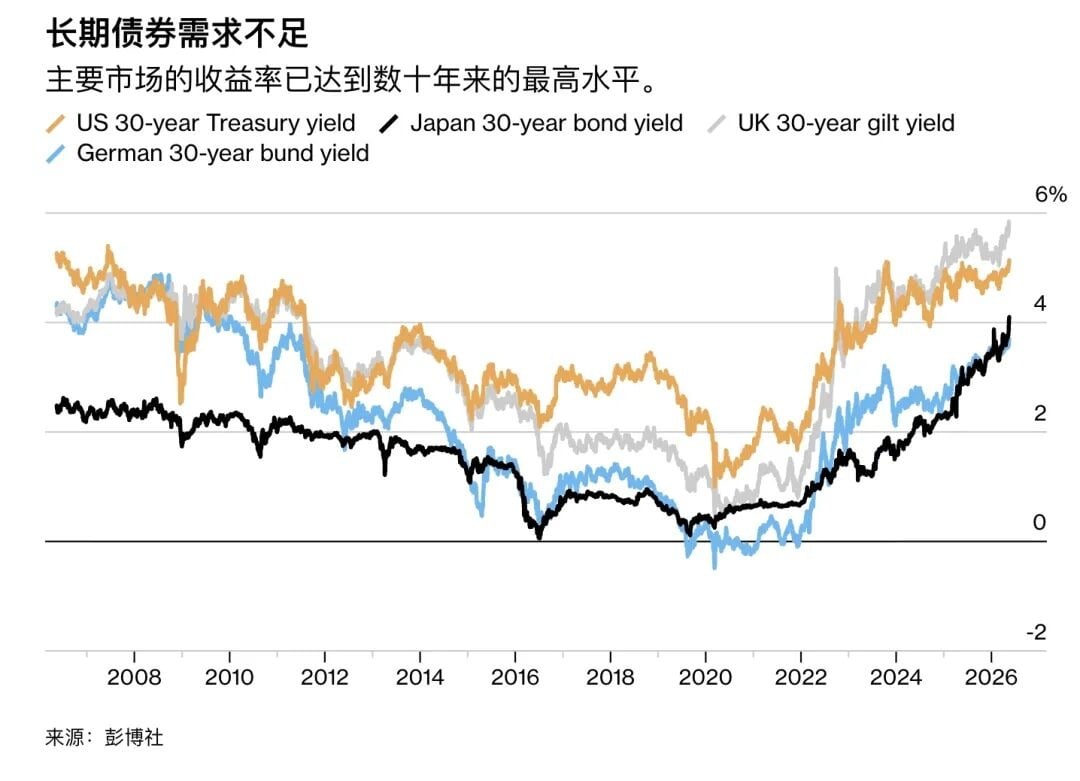

On Monday (May 18), during Tokyo's early trading, the Japanese bond market underwent a significant adjustment, with the yield on the ten-year government bond reaching 2.797%, breaking a nearly thirty-year market record, marking the highest point since October 1996. Previously, the yield on U.S. thirty-year government bonds had also surpassed the 5% threshold, touching 5.12% in actual trading, reaching a new high since 2007.

The situation is not just bad for U.S. and Japanese bonds.

The yield on French thirty-year government bonds reached as high as 4.675%; German thirty-year government bonds hit 3.704%; and British thirty-year government bonds soared to 5.86%.

By Monday, although the volatility in the bond market had eased compared to the market crash on Friday, it remained hovering around multi-year highs.

This wave of selling triggered by the global bond market has threatened global stock markets. Morgan Stanley warned that if volatility in the bond market escalates further, U.S. stocks will face their first meaningful adjustment, leading to the end of the entire AI bull market.

High bond yields drag down the stock market

Bond market loses the "Maginot Line"

In the bond market, bond yields and prices are negatively correlated—the more bonds investors sell, the higher the yields.

Michael Hartnett, Chief Strategist at Bank of America, believes that when the yield on thirty-year U.S. government bonds crosses 5% and the yield on ten-year U.S. government bonds exceeds 4.5%, it signals danger. He referenced historical experience from the past hundred years, suggesting that when inflation crosses this threshold, capital markets may trigger large-scale deleveraging shocks, and risk assets often enter a correction phase, with the S&P index averaging a 4% drop in the following three months and a 7% drop within six months.

Thus, these two levels have become the "Maginot Line" of the bond market.

Now, this line has already been breached.

So, who is the culprit behind the breach of the bond market line?

The answer is straightforward: the energy prices that have gradually desensitized the market over the past month.

Due to the substantial breakdown of negotiations between the U.S. and Iran, coupled with the ongoing blockade of the Strait of Hormuz, international oil prices have surged significantly, with Brent crude oil surpassing $110 once again as of the early hours of May 19.

Brent crude oil breaks $110 again

This has initiated a familiar chain of transmission: Middle Eastern geopolitical crisis → global inflation reignited → U.S. Federal Reserve's reversal of expectations → bond market sells off.

On one hand, inflation reignited in Europe and the U.S. For example, the U.S. Department of Labor reported that in April, the Consumer Price Index (CPI) rose by 3.8% year-on-year, up from 3.3% in March, reaching the highest level since June 2023. The Producer Price Index (PPI) in the U.S. also rose by 6% year-on-year in April, the highest level since December 2022.

Moreover, data from the prediction platform Kalshi indicates that the probability of the U.S. economy facing stagflation before the end of this year has risen from 11% to 40%.

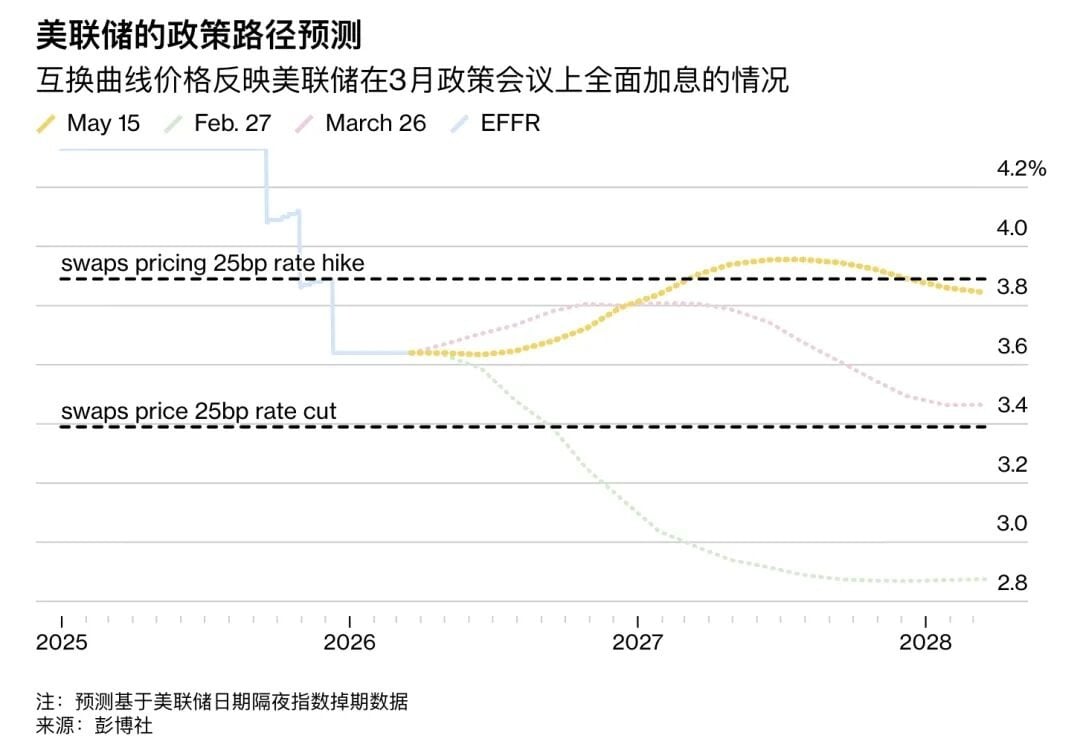

On the other hand, high inflation data has completely reversed the market's judgment on the Federal Reserve's policy path.

In the face of stagflation threats, the Federal Reserve may not only refrain from further interest rate cuts but may instead plan for rate hikes—market predictions indicate that the probability of rate hikes before July 2027 has risen to 60%, meaning the market will quickly sell off bonds under the Federal Reserve's rhythm, further pushing up government bond yields.

As the transition of the Federal Reserve Chairman occurs at a critical juncture, the first task of the newly appointed Fed Chairman Waller may be to closely monitor the bond market and maintain strict vigilance over inflation issues.

Dongwu Securities believes that the trajectory of the U.S.-Iran conflict will dictate the short-term trends of U.S. treasury yields; key attention can be paid to any turning points in the U.S.-Iran conflict, oil prices, and the PCE data in late May. In the long term, as the expectations of interest rate hikes by the Federal Reserve strengthen, focus should shift towards AI-driven industries and the resilience of U.S. economic growth.

High interest rates discount technology stocks

So why do large fluctuations in the bond market lead to a drop in the stock market?

The rise in U.S. treasury rates means higher market risk-free rates, which in turn raises the discount rate for technology stocks, causing the valuations of U.S. technology stocks to collapse.

The so-called "discount rate" refers to the interest rate used to convert future cash flows into present value, and it equals the risk-free rate + risk premium. The higher the discount rate, the lower the current value of the same amount of money; for AI technology stocks, most of their value lies in the distant future.

Thus, when U.S. treasury yields rise, the discount rate increases, discounting future earnings more harshly, delivering a heavy blow to technology stocks that rely heavily on future cash flows.

This is also why, in the past, when the Federal Reserve has hinted at rate hikes or long-term bond yields have surged, the Nasdaq index often takes the lead in plummeting.

Similarly, fluctuations in bond yields exert a valuation restraint on technology stocks in the A-share market.

Calculated based on the yield of ten-year treasury bonds, on May 18, the yield on U.S. ten-year treasury bonds was 4.63%, while China's ten-year treasury bond yield was 1.76%, with a spread of 2.87%. When the spread between U.S. and Chinese treasury yields widens, it means that the attractiveness of risk assets in emerging markets like China declines relatively.

As investors, if you can get a 5% yield from U.S. treasury bonds, why take on the exchange rate and investment risks in emerging markets for uncertain yields?

China Securities Journal quoted industry insider opinions, pointing out that rising government bond yields pose significant pressure on technology sectors represented by artificial intelligence; the increase in bond yields undermines investors' motivation to hold stocks. Furthermore, rising international oil prices further strengthen expectations of interest rate hikes, suppressing market risk appetite for technology stocks.

On May 16, the Tokyo stock market's Nikkei index closed

However, everything is not yet concluded. Goldman Sachs strategist Rich Privoratki believes that the core contradiction in the current market lies in the direct confrontation between the bond market and the AI boom, much like an ongoing tug-of-war.

On the AI front, strong industry demand has led relevant technology stocks to achieve performance beyond expectations, becoming a continual and stable support for the near future. According to research from CICC: the S&P 500's first-quarter earnings growth rate reached 28%, the highest since the fourth quarter of 2021, with the semiconductor and equipment sectors experiencing growth of up to 99%. The situation in the A-share market is similar; data shows that in the first quarter of 2026, the semiconductor equipment sector's revenue reached 25.498 billion yuan, a year-on-year increase of 25.78%, with net profit attributable to the parent company at 4.446 billion yuan, a substantial increase of 60.42% year-on-year.

At the same time, the AI boom itself also accumulates significant risks, which is the underlying reason for the bond market's fluctuations triggering shocks.

Previously, UBS had issued a clear warning that the prices of AI-related stocks and large technology stocks are already extremely high, and their growth expectations far exceed the actual levels. Research from the bank indicated that major technology stocks, including the "big seven tech giants," exhibit an overly bullish phenomenon. Legendary investors Jim Rogers and Michael Burry, who predicted the 2008 subprime mortgage crisis, have both called for investors to cut their holdings of technology stocks and issued warnings against the frenzy surrounding AI.

How should ordinary investors respond to new changes?

Ray Dalio, founder of Bridgewater Associates, stated in April that the world is entering a new era dominated by the "law of the jungle," and investors must revisit their wealth protection strategies.

In light of some new changes currently, we have distilled some of the latest institutional opinions for reference:

Xinyuan Fund believes that for the future trends of the A-share market, there has not been a trend change in the liquidity environment; last week's market was more a high volatility disturbance and emotional shock, rather than the beginning of systemic risk. It is recommended that investors increase flexibility and retain more tactical positions to cope with the high volatility environment brought by rising U.S. treasury yields. In terms of sectors, attention can continue to focus on the AI industry chain, including domestic computing power, optical modules, semiconductor equipment, and related machinery and chemical new materials.

Huatai Securities believes that the A-share sentiment index has been operating in the overheating zone for two weeks, with the valuation differentiation coefficient approaching the high level of 2021, and rebalancing pressure between sectors is rising, indicating high probability of adjustments using time to exchange for space. In terms of allocation, the technology main line, such as communication equipment and storage, can continue to hold; within technology, consideration can be given to switching to semiconductor (core stock) equipment and discrete devices.

The ambiguous geopolitical crisis and the sweeping artificial intelligence revolution are placing the global market in an awkward position, whether to cash out or make a bold advance, investors may need to do their homework moving forward.

As John Templeton, the "father of global investing," once said: "Bull markets are born in pessimism, grow in skepticism, mature in optimism, and die in frenzy."

Disclaimer: This article represents only the personal views of the author and does not represent the position and views of this platform. This article is for information sharing only and does not constitute any investment advice to anyone. Any disputes between users and authors are unrelated to this platform. If the articles or images on the webpage involve infringement, please provide relevant proof of rights and identity documents and send an email to support@aicoin.com. The relevant staff of this platform will conduct an investigation.