Author: Dragonfly

Compiled by: Felix, PANews

Reliable salary data in the crypto space is extremely scarce. Dragonfly previously released the first salary-related dataset and analysis report (2023). Now, Dragonfly has released another salary report, covering 85 cryptocurrency companies, with data collected at the end of 2024 and the first quarter of 2025. This report also expands the scope of research, including data from approximately 3,400 independent and non-redundant employees and candidates, and compares the findings with the 2023 report where relevant. This article highlights key excerpts from the report, with the following details:

Highlights

- Most crypto companies are in growth mode, but not in high-growth mode.

- Recruitment in the crypto industry has been global from the start, with almost no recruitment limited to the United States.

- Europe is a major international hub.

- Base salaries and token compensation have declined across almost all levels and regions.

- Remote work remains prevalent, and major companies do not intend to change this status quo.

- The crypto industry is difficult to enter, with less than 10% of positions being entry-level.

- The engineering department dominates.

- Salaries in the U.S. set the standard for global engineering leadership positions.

Compensation Status

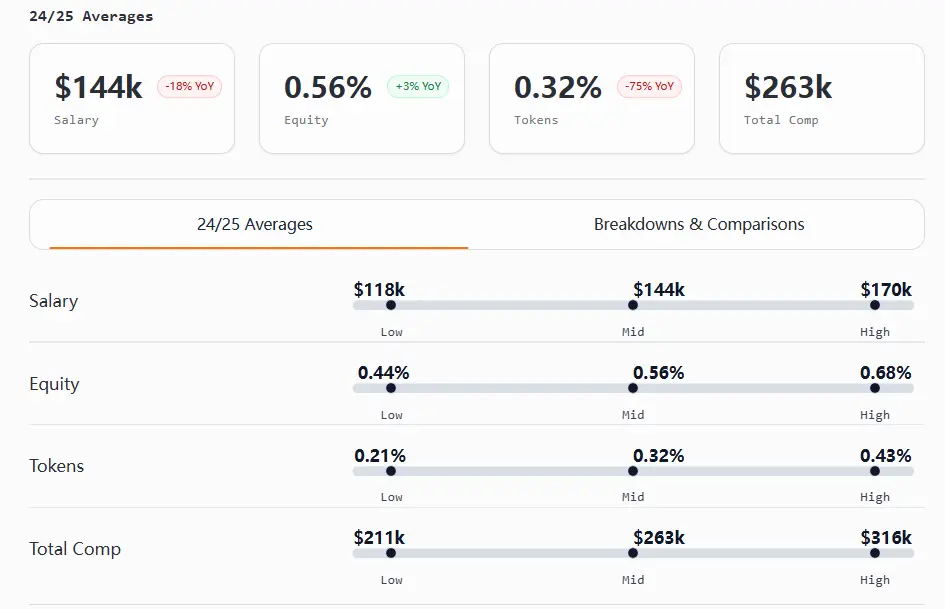

Overall, salaries in the crypto industry at the end of 2024 and early 2025 are in a downward market, and compared to traditional industries, their compensation systems remain relatively immature.

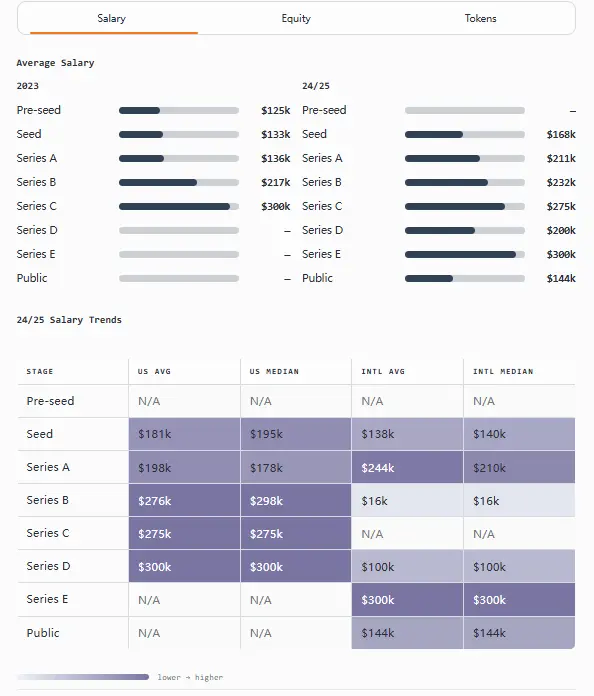

Salaries and token rewards have declined across almost all levels. Cash compensation for U.S. positions remains leading, while international teams narrow the gap by offering larger equity and token rewards. Equity distribution is uneven, especially for non-technical, non-executive positions. Salary ranges in the U.S. have narrowed, while international positions can sometimes reach 2 to 10 times the U.S. level.

Divided by development stage, the expected pattern still holds: early-stage companies offer lower salaries but more equity (usually double), while later-stage teams do the opposite. Tokens have generally become less common but still hold significant importance in go-to-market (GTM), product, and senior international positions.

Entry-level positions are hit the hardest, with significant salary declines and reduced bonuses, although equity rewards have increased. Cash income for new hires in the U.S. remains high, but international counterparts typically receive 2 to 3 times the equity and more token rewards.

Mid-level employees are squeezed, with limited growth, while senior employees fare better, experiencing smaller pay cuts, more stable equity, and increasingly concentrated token rewards at the top.

Senior individual contributors (ICs) and executives see the largest salary increases, particularly evident in product and engineering fields.

Compensation Benchmarks

Below are salary data for various positions including software engineering, crypto engineering, developer relations, product management, design, marketing, and market expansion.

International engineering executives' compensation has surpassed that of their U.S. counterparts for the first time (total compensation ranging from $530,000 to $780,000), thanks to a nearly 3% increase in token rewards.

For crypto engineers, the trade-off between "certainty and upside potential" is clearer than ever. U.S. engineers lead in cash and total compensation at almost every level, while international counterparts excel in equity and token rewards at entry and mid-levels.

Product management executives have the highest salaries among all positions ($390,000 to $484,000), with total compensation comparable to or higher than engineering positions; international product management equity rewards are typically about 2 to 10 times that of the U.S. level.

Developer relations has become the most "borderless" function, with global salary ranges nearly identical, and minimal differences at the manager and executive levels (U.S. leads in equity and total compensation; international leads in tokens).

Leadership in design roles is not as valued as senior designers. U.S. design ICs (chief/senior) exceed managers in total compensation, even surpassing some executives.

Marketing shows regional disparities in compensation and ownership. The U.S. leads in salary and total compensation, while international companies' equity is about 3 to 10 times that of the U.S. level.

GTM total compensation sees a narrowing pay gap at entry and manager levels. Senior ICs exceed managers in total compensation, while leaders in international business units excel in equity.

Founder Compensation

In this report, company ownership is divided into equity and tokens (unlike previous reports where they were combined). Therefore, salary analysis is reported year-over-year, while equity and token data reflect the 2024/2025 figures.

Compared to last year, founder compensation has increased. Overall, the higher the funding amount, the higher the salary, and the lower the equity share (as expected).

U.S. founders generally earn more than their international counterparts in salary, equity, and tokens.

Key Points:

- Founders' average salary has increased by about 37% year-over-year, from $144,000 in 2023 to $197,000 in 2024/2025.

- U.S. founders in the seed round have the highest equity share (32%).

- In the seed round stage, the proportion of token holdings is relatively stable across regions (9%), but significant differences arise in later stages.

- Rare exception: In Series A funding, international founders report higher salaries than U.S. founders ($244,000 vs. $198,000), while U.S. founders hold more tokens (13% vs. 9%) and slightly more equity (20% vs. 19%).

- Rare exception: In Series B funding, international founders report the highest equity share (30%), but this data is based on limited information and should be interpreted cautiously.

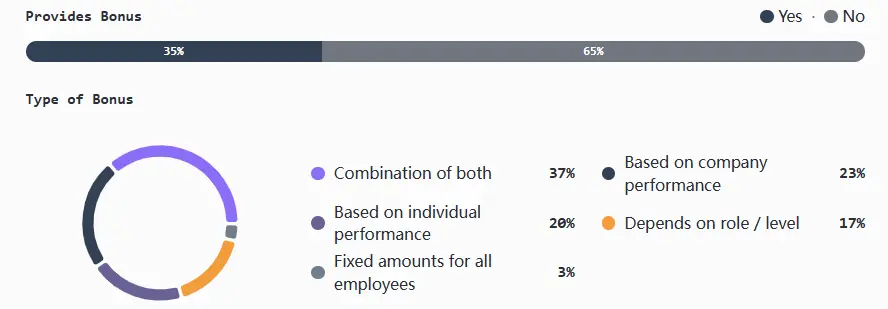

Bonuses and Variable Compensation

The use of bonuses decreases as companies grow: smaller and early-stage teams are most likely to experiment, mid-sized companies adopt selectively, while later-stage and infrastructure-oriented companies gradually reduce usage in favor of long-term incentives.

When bonuses are present, they are typically tied to company and individual performance (mixed). Models tied only to company performance, only to individual performance, or based on position/level are less common, and fixed bonuses are rare.

Key Points:

- Bonuses peak in the smallest companies (1-5 employees) and early stages (seed/A round), especially in companies with funding amounts between $5 million and $19.9 million.

- CeFi has the highest adoption rate at 71%; DeFi is at 50%, primarily driven by the U.S. and focusing more on individual performance; infrastructure/L1/L2 has a much lower adoption rate (15-30%) and typically uses a mixed model.

- The U.S. offers more favorable bonus arrangements, especially for mid-sized teams.

- Exception: Some well-funded post-Series C teams report facing "overwhelming applications" due to increased hiring demand and enhanced brand recognition.

- Exception: Infrastructure companies face the broadest challenges: 63% mention talent shortages, 27% mention compensation issues, 5% mention competition, and 5% mention remote/global hiring (the only area mentioning this issue).

Token Compensation Analysis

Many teams are increasingly separating tokens from equity when calculating token grants. In later stages, the common practice is to link grants to fair market value, most commonly using time-weighted average price (TWAP).

In terms of vesting, most teams follow a four-year plan with a one-year "cliff," but some teams have experimented with mixed models that combine time-based and milestone-driven unlocks.

Most companies issue tokens from dedicated employee token pools, with only a few very large organizations still allocating grants from total supply, which is becoming increasingly rare.

Compensation Composition (Cash, Tokens, Equity)

Early teams heavily rely on equity to maintain token flexibility. Mid-sized organizations typically shift to a mixed model (equity + tokens), providing risk-adjusted compensation structures and additional liquidity. Most later-stage companies tend to revert to equity once company value and token liquidity dynamics stabilize.

Key Points:

- Nearly half of international teams (44%) only offer tokens. U.S. teams, in contrast, have only 39% that offer only equity.

- Early companies heavily rely on equity (about 71% when employee count is 1 to 5), with mixed compensation peaking in Series A and gradually shifting towards equity (45% in Series B, 71% in Series C).

- Protocol-intensive fields like L1, L2, and DeFi naturally lean towards token-dominant compensation, while infrastructure, consumer, and CeFi companies default to equity.

- Among teams before TGE, nearly one-third only offer equity and token payments, with mixed payments at 32%; once projects launch, teams heavily rely on token payments (47% offer only token payments, 47% offer mixed payments), with pure equity payments nearly zero.

- Rare exception: A very small number (5%) only offer cash payments.

Equity/Tokens Relationship (Ratio)

Only a few teams establish a ratio relationship between equity and tokens, meaning the company determines future token grants based on individual equity shares.

This was the norm before TGE, but as companies mature, almost all have severed this connection. In later stages, equity and tokens are viewed as entirely separate entities.

Key Points:

- 51% of companies view tokens and equity as independent compensation elements (no ratio connection); this has become common by Series D and beyond.

- In the seed round/TGE early stages, ratio models remain the most common (33%), but overall, their usage has declined as companies develop.

- Case: 90% of L2 companies have no ratio relationship and no uncertain status.

- Region does not affect the ratio relationship.

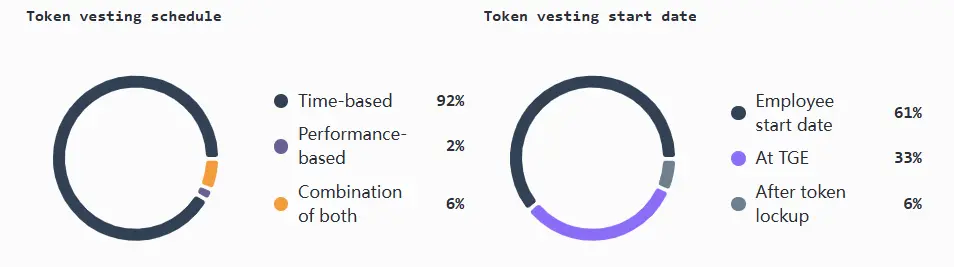

Vesting Schedules and Start Date Practices

Before TGE, companies (especially in the DeFi and L1 sectors) typically start vesting at TGE to manage retention and circulating supply. Teams with circulating tokens usually begin vesting on the employee's start date (the most common method). These practices are largely consistent between U.S. and international teams, with the main differences seen in teams before TGE.

Most companies adopt standard time-based vesting, usually a four-year plan with a one-year "cliff."

A few teams explore performance-linked vesting or a combination of performance and time. It is reported that teams are cautious about linking vesting to network-level KPIs (which individuals find hard to control) and instead focus on auditable product, team, and individual milestones.

Key Points:

- 61% of companies start vesting on the employee's start date.

- 59% of pre-TGE teams start vesting at TGE.

- Vesting arrangements are mostly standardized, with 92% of companies using time-based vesting, typically completed within 4 years, with the first year as a "cliff."

- Exception: Only a few companies deviate from standard time-based vesting: 6% use a mixed time and milestone model, and 2% rely entirely on performance-based arrangements.

Geography and Remote Work

Recruitment Footprint

Global priority is the default mode, with most teams recruiting internationally from day one. Generally, talent acquisition and flexibility are more important than geographic location.

Recruitment limited to the U.S. is rare, mainly occurring in seed and Series A rounds, and this practice gradually disappears as companies grow. Recruitment limited to international candidates remains stable across various stages and sizes of companies, often reflecting cost-sensitive hiring strategies.

Key Points:

- From day one, globalization becomes the default choice, with 81% of companies recruiting simultaneously in the U.S. and globally.

- Smaller teams tend to start global recruitment earlier. Companies with 21 to 100 employees and funding between $20 million and $40 million are the most stable, even more so than larger companies.

- Infrastructure teams are most likely to engage in global recruitment, with a rate of 80%.

- Rare exceptions: Recruitment limited to the U.S. is almost nonexistent, accounting for only 6%, primarily adopted by early consumer and DeFi teams, but they abandon this practice as they scale.

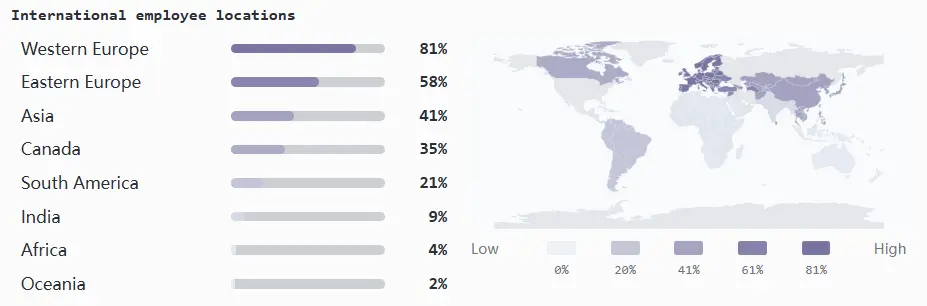

Location of International Employees

Western Europe is a major international recruitment hub.

As companies mature, there is a need for stronger local operations, typically leading to a shift towards regional recruitment in the later stages of Series B, expanding into Asia, Canada, and Eastern Europe.

Key Points:

- Western Europe: 84% of companies in Series B to E (and approximately the same proportion of those with over $40 million in funding) have hired employees locally.

- Eastern Europe: 63% of later-stage companies recruit here, attracted by a strong engineering talent pool and cost-effectiveness.

- Asia: Recruitment rates have nearly doubled year-on-year (from 20% to 41%) to accommodate stronger market applications.

- Canada: 38% of companies in Series B to E are expanding into Canada, leveraging its proximity to the U.S., favorable regulatory environment, and developer base as a hedge.

- South America: Only 13% of companies in Series B to D are expanding here.

- Rare exceptions: India (9%), Africa (4%), and Oceania (2%) remain underdeveloped.

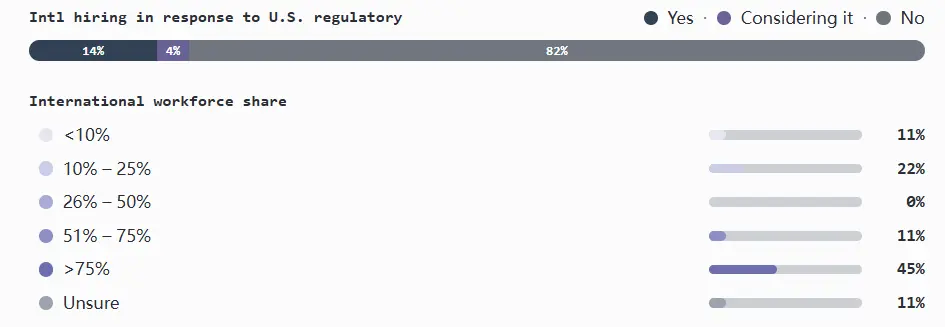

Regulatory-Driven Recruitment Changes

From 2023 to 2024, regulation has become one of the hottest external factors influencing crypto talent strategies. In the U.S., increased scrutiny around trading, custody, and protocol activities has made compliance considerations significant in hiring decisions.

However, looking back at early 2024 and 2025, the impact of regulation on prompting companies to hire outside the U.S. has been minimal. Adjustments have mainly focused on larger, better-funded teams in the infrastructure and DeFi sectors (which are most likely to hold or issue tokens) and in the CeFi sector (which faces stricter regulation).

Companies with both U.S. and international teams are most likely to mention regulatory-driven initiatives, while those operating solely in the U.S. generally do not respond, with only a few considering changes.

Key Points:

- Overall, only 14% of companies have adjusted their hiring strategies due to regulatory pressure.

- Nearly a quarter of companies with employees in both the U.S. and abroad state that regulation directly prompted their decision to expand international hiring.

- Among companies with only international employees, most have globalized for other reasons, but 21% acknowledge that regulation has played a role.

Remote Work and Hybrid Work Policies

The crypto industry remains predominantly remote, with most companies adopting a fully distributed work model. The second most common is a hybrid model, combining remote work with mandatory office attendance. The remote-first (optional office attendance) model occupies a small middle ground, with very few companies operating entirely in-office.

Both models are strongly ideated, and overall, policies are difficult to change: almost all teams plan to maintain their current models.

Key Points:

- Over half of the companies operate fully remotely, more than a quarter adopt a hybrid model, while remote-first companies make up a smaller proportion at 14%.

- 94% of companies have no plans to change their policies.

- U.S. teams are more inclined towards remote work (55%), while international counterparts prefer hybrid work (35%).

- Series A funding teams have a relatively hybrid work style, but by Series B funding, remote work accounts for 73%.

- Rare exceptions: Only 2% of companies operate entirely in-office.

Organizational Structure and Recruitment Trends

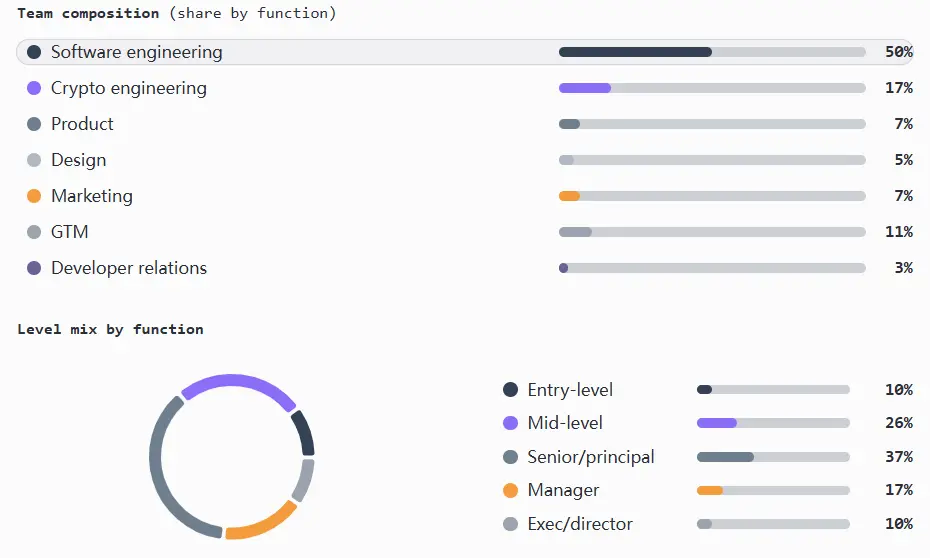

Team and Level Composition

The crypto industry has long been dominated by engineers, a trend reflected across various sizes, stages, and funding levels from pre-seed to post-Series B. International teams tend to favor engineers, while product and marketing leadership positions are primarily concentrated in the U.S.

From a team growth perspective, seed round teams are mainly engineers; Series A to B sees an increase in senior product managers, designers, and marketing teams (with fewer managers); post-Series B, there is an increase in architecture in marketing and engineering.

Notably, entry-level position recruitment is scarce, limiting talent pools and diversity, making it harder for newcomers to enter the industry (especially in product and marketing). Executive recruitment outside of engineering is also very limited.

Key Points:

- Engineering (software and crypto) positions account for about 67% of total employees across companies of different sizes, stages, and funding rounds.

- Entry-level positions make up only 10% of all positions.

- The product department is understaffed, with over half of product managers at senior or executive levels.

- The marketing department is also small, accounting for only 7% of total employees, with a slightly higher proportion in international teams.

- The GTM department accounts for 11% of total employees, primarily in mid to senior positions.

- The developer relations department accounts for 3% of total employees, mainly in mid-level positions, with compensation comparable to other departments.

- The design department is primarily senior, lacking leadership, with about 44% at senior levels and fewer than 10% in manager or executive roles.

- Other departments, aside from engineering, are leanly staffed: the marketing/engineering ratio is 1:14, and the product/engineering ratio is 1:13.

- Rare exceptions: In some international teams, the ratio of product managers to engineers can be as high as 1:20.

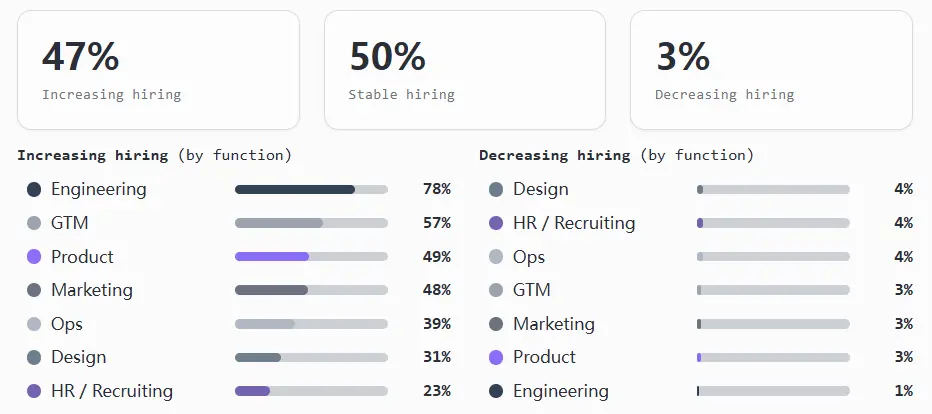

Recruitment Momentum by Function

Most teams are in a target growth mode rather than hyper-growth. Overall, companies are streamlining support teams while selectively expanding core teams, with many companies intending to maintain headcount, and few planning to reduce overall staff numbers.

Recruitment momentum aligns with the aforementioned team composition. The engineering department is clearly a priority, while product and marketing departments are growing steadily but cautiously. In expansion phases, as well as in infrastructure and finance sectors, GTM (sales, marketing, and operations) recruitment momentum is strong, but it slows down in consumer, gaming, and NFT companies. The design department remains underdeveloped, while operations and HR/recruitment departments are roughly even, potentially causing bottlenecks due to the faster growth of technical teams compared to internal support.

Key Points:

- The engineering department leads growth, with about 78% of teams expanding, and only 1% of teams downsizing. This is also the only department with a genuine entry-level recruitment channel.

- GTM recruitment increases with the growth stage, with 57% of teams expanding and 40% maintaining.

- Product and marketing departments remain stable, with about half of teams increasing and half maintaining.

- Few teams are expanding comprehensively; most teams expand in 2 to 4 functions while keeping others unchanged, likely to simplify the hiring process.

- GTM will only expand if senior and executive talent is already in place, and companies rarely recruit entry-level positions.

- Slow growth often accompanies teams with a high proportion of senior talent; once senior and executive levels in product, design, or engineering are in place, these departments are more likely to stabilize and slow down hiring.

- Overall layoff rates are low, at 3%, with slightly higher layoff rates in design, operations, and HR/recruitment departments.

Related reading: a16z on Hiring: Crypto Native vs. Traditional Talent, Who's Worth Betting On?

Disclaimer: This article represents only the personal views of the author and does not represent the position and views of this platform. This article is for information sharing only and does not constitute any investment advice to anyone. Any disputes between users and authors are unrelated to this platform. If the articles or images on the webpage involve infringement, please provide relevant proof of rights and identity documents and send an email to support@aicoin.com. The relevant staff of this platform will conduct an investigation.