Playing with Boros' yield space can even be more profitable than Meme.

If you were to nominate the most innovative DeFi protocol, who would you choose?

Pendle must surely be on the list.

In 2021, Pendle, as the first DeFi protocol to focus on the "interest rate swap" market, single-handedly opened up a yield trading market worth billions, becoming the absolute leader in the yield trading sector.

And in August 2025, Pendle's innovative core of "daring to be the first" continued with the launch of Boros, opening up the on-chain yield blind spot of "funding rates," bringing trading, hedging, and arbitrage opportunities for funding rates to the DeFi world for the first time, once again sparking public discussion and a surge in participation.

According to the latest data from Pendle, as of now, Boros has been online for two months, with a cumulative nominal trading volume exceeding $950 million, an open contract size exceeding $61.1 million, and the number of users surpassing 11,000+, with an annualized income exceeding $730,000.

In just one month, it has achieved what many projects take years to accomplish, and many participants excitedly express: Playing with Boros' yield space can even be more profitable than Meme.

So, what is Boros? How to play it? What are the future plans?

Many people may have noticed that Boros' brand visuals often feature a giant whale that devours everything, and the term Boros in ancient Greek also means to devour. With the release of Boros 1.0, the launch of the referral program, and more markets being introduced, perhaps Boros' devouring of the yield world is officially unfolding through funding rates.

Why is "funding rate" the first shot to establish Boros' product reputation?

As a structured interest rate derivatives platform, Boros currently focuses on funding rates, aiming to transform funding rates into tradable standardized assets.

Most contract users are likely familiar with funding rates; they act like an "invisible hand" in the contract market, balancing perpetual contract prices with spot prices. The specific operational logic can be simply understood as:

When the funding rate is positive, it indicates that most people expect prices to rise, with the bulls being strong, causing contract prices to be higher than spot prices. Bulls must pay the funding rate to bears, suppressing excessive optimism in the market.

When the funding rate is negative, it indicates that most people expect prices to fall, with the bears being strong, causing contract prices to be lower than spot prices. Bears must pay the funding rate to bulls, suppressing excessive pessimism in the market.

As a key to balancing long and short forces, funding rates are also a crucial indicator of market sentiment.

Before Boros appeared, traders passively accepted the market's regulation through funding rates, never considering that one day funding rates could also become a separately tradable asset.

So, why did Boros choose funding rates as the first shot to establish its product reputation?

High scale, high volatility, and high yield—these characteristics unique to funding rates are the fundamental reasons Pendle believes they hold great potential.

- High scale:

The scale of the contract market has far exceeded that of the spot market, and once the contract market operates, funding rates flow continuously.

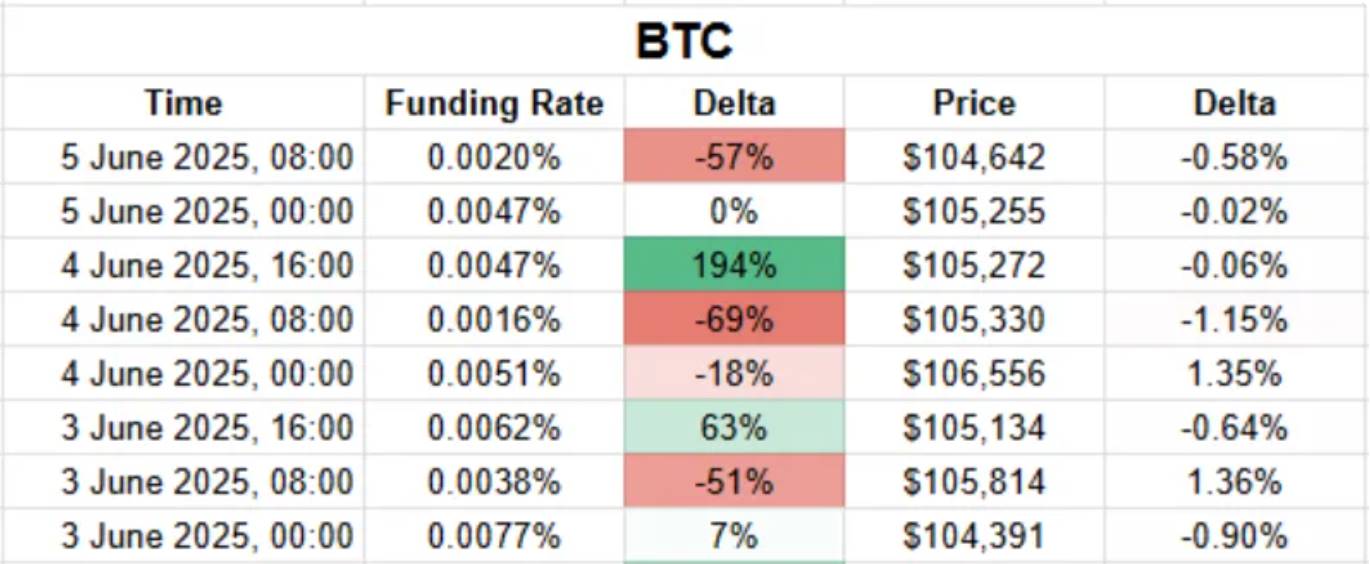

According to a CoinGlass report, the total trading volume of perpetual contracts in Q2 2025 reached $12 trillion, with an average daily trading volume of about $130 billion; based on the settlement rules of most exchanges at 0.01% / 8 hours, the daily funding rate market easily exceeds tens of millions, and in extreme market conditions, it can even exceed hundreds of millions.

If we can better utilize this vast and stable market of funding rates, it will undoubtedly give rise to the next heavyweight financial innovation.

- High volatility:

In the spot market, tokens can experience significant price fluctuations within a day, but this is the norm in the funding rate market.

For example: According to Coinmarketcap data, on September 8, 2025, MYX Finance (MYX) surged over 168.00%, becoming the top gainer among the top 100 cryptocurrencies by market cap and quickly becoming a hot topic in the market. Meanwhile, in the tug-of-war between bulls and bears, funding rates themselves are constantly fluctuating, especially for many altcoins, where the volatility of funding rates can reach four to five times or even more. For instance, some traders paid as high as 20,000% annualized funding rates to maintain long positions in $TRUMP.

Taming the volatile beast of funding rates will not only help users better formulate trading strategies but also hide enormous profit opportunities.

- High yield:

The core logic is: volatility creates excellent opportunities for profit.

With volatility, there is room for buying low and selling high. The highly volatile funding rate market can also become an important avenue for users to capture profit opportunities.

How to transform funding rates into a standardized asset to achieve trading, profit, hedging, and arbitrage strategies is a significant test of product design skills.

How does Boros achieve betting on the future rise and fall of funding rates?

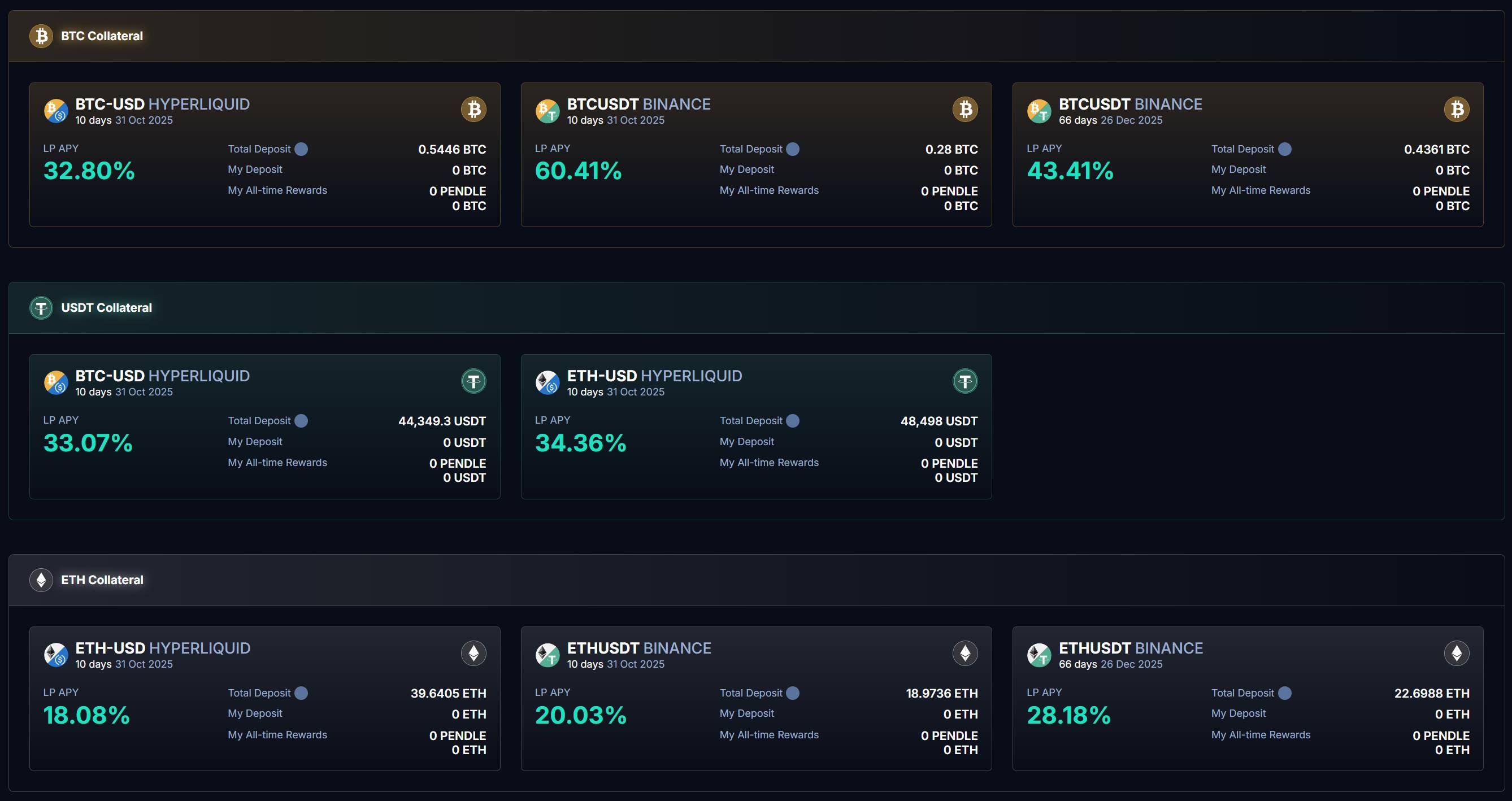

Entering the Boros page, we can see that Boros has currently launched multiple markets for BTC, ETH, and USDT on Binance and Hyperliquid:

As mentioned earlier, funding rates are a key indicator of market sentiment. In other words, if you can accurately sense market sentiment, you can profit through Boros' funding rate trading.

So how can we turn this market prediction into tangible profits?

The core of Boros lies in fixing the current funding rate of the market and using it as a benchmark to provide users with betting options: if the rate rises in the future, the bulls profit; if the rate falls in the future, the bears profit.

All of this is achieved through YU.

Users can connect their wallets to deposit collateral and purchase YU.

YU is the core means of transforming funding rates into a standardized asset, representing the right to the yield of funding rates over a certain period in the future. At the same time, YU is also the smallest trading unit after quantifying funding rates. For example, purchasing 1 YU BTCUSDT Binance means representing the yield of the funding rate for a 1 BTC position on Binance's BTCUSDT.

We know that yield = income - cost. The yield calculation for YU relies on three core data points: Implied APR, Fixed APR, and Underlying APR.

Buying YU is equivalent to opening a position, which includes two parts of cost:

On one hand, Implied APR is the rate locked in when opening a position, which can be seen as the price of YU, serving as the fixed annualized rate before expiration. Implied APR is a benchmark for measuring future changes in market funding rates, representing the fixed annualized rate of funding rates over a certain period in the future.

On the other hand, opening a position requires transaction fees, which, along with Implied APR, make up the Fixed APR, i.e., the cost of opening the position.

Once the costs are clear, we can calculate the income.

By purchasing YU, we have fixed a funding rate, while the actual funding rate on external exchanges is represented by Underlying APR.

When purchasing YU, we have two options to achieve long/short positions on funding rates:

Buy Long YU (betting on rising funding rates): During the expiration period, the user pays Implied APR and receives Underlying APR.

Buy Short YU (betting on falling funding rates): During the expiration period, the user pays Underlying APR and receives Implied APR.

At this point, the yield exists in the difference between income and cost, which is the difference between Fixed APR and Underlying APR.

When Fixed APR < Underlying APR, i.e., when the market floating rate is higher than the fixed rate, Long YU users profit.

When Fixed APR > Underlying APR, i.e., when the market floating rate is lower than the fixed rate, Short YU users profit.

This leads to:

Betting on rising funding rates: buy Long YU.

Betting on falling funding rates: buy Short YU.

In terms of yield settlement, Boros synchronizes with the settlement cycle of perpetual contract trading platforms.

Taking the currently launched BTCUSDT Binance product as an example: Binance's funding rate settles every 8 hours, and Boros' BTCUSDT Binance trading pair also settles every 8 hours.

At each settlement, Boros calculates the difference between Fixed APR and Underlying APR for settlement:

When Fixed APR < Underlying APR: deduct collateral from Short YU and distribute the yield to Long YU users.

When Fixed APR > Underlying APR: deduct collateral from Long YU and distribute the yield to Short YU users.

We know that YU represents the right to the yield of funding rates over a certain period in the future, and this yield right settles every 8 hours (or 1 hour) according to exchange rules. This means that the value of YU will decrease with each settlement, ultimately returning to zero after expiration when it no longer predicts the funding rate price.

Of course, to leverage a larger yield space, Boros also provides leverage tools of up to 3 times, allowing users to open larger positions with less collateral, but high leverage also comes with greater liquidation risks. Users need to regularly monitor their health factors and adjust their collateral in a timely manner to avoid liquidation.

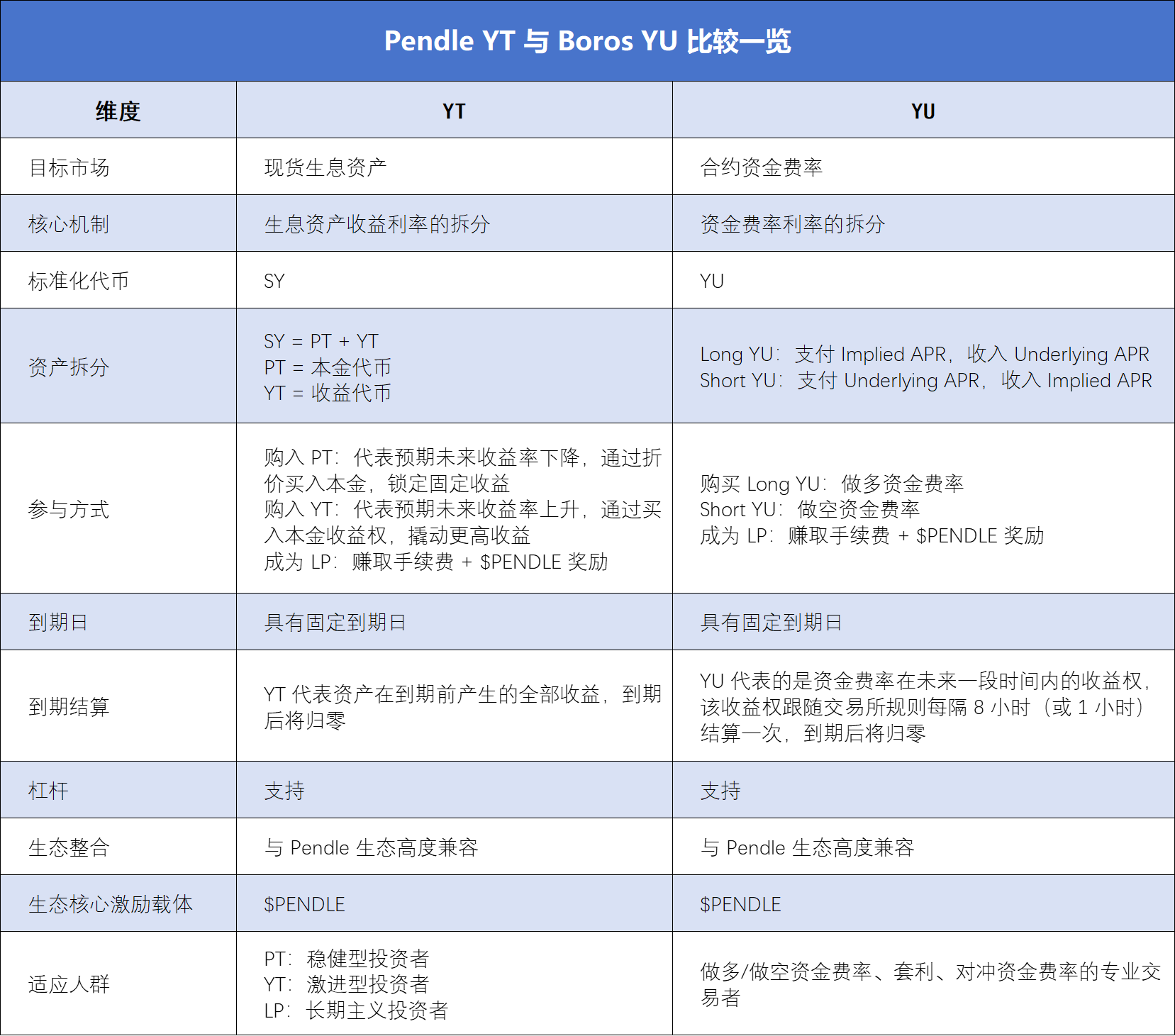

For many who are familiar with Pendle's YT rules, there are indeed many similarities between YT and YU that can help users deepen their understanding of YU. However, there are also significant differences between the two, which we can clarify through the table below:

From Hedging to Arbitrage: Boros Becomes a Cost-Reducing and Efficiency-Enhancing Tool for Traders

Based on this set of strategies for betting on the rise and fall of funding rates, Boros has sparked spontaneous discussions among contract traders, institutions, and professional DeFi players since its launch, actively exploring the practical applications of Boros in various scenarios.

The most direct way to participate is to buy YU to bet on the fluctuations of funding rates:

In the choice between Long YU and Short YU, users can earn the difference between fixed and floating rates. On September 12, 2025, Boros launched the funding rate trading market on Hyperliquid, which has greater volatility compared to Binance, providing users with a stronger betting experience.

For long position holders, Boros's greater utility lies in hedging funding rates in a high-volatility environment: By adopting a rate strategy opposite to that of CEX perpetual positions on Boros, users can offset the volatility risk of floating rates, thereby locking in costs/returns as a fixed value.

For example, if a user holds a long position in CEX and pays the floating rate, they can buy Long YU on Boros, which offsets the floating rate paid to CEX with the floating rate income from Boros.

Conversely, if a user holds a short position in CEX and pays the floating rate, they can buy Short YU on Boros, which offsets the floating rate paid to CEX with the fixed rate income from Boros.

This way, the risks and costs of contract trading become more controllable, which is very attractive for traders, especially institutional traders. A very intuitive case is Ethena: as one of the representative projects of delta-neutral strategies, Ethena's revenue mainly comes from positive funding rates. Therefore, when funding rates fluctuate dramatically, Ethena also faces significant revenue uncertainty, which can even affect the project's sustainable development.

Through the YU of the Boros protocol, Ethena can lock in a fixed rate on-chain, achieving predictable returns and thereby enhancing the protocol's profitability stability and efficiency.

At the same time, the launch of the Hyperliquid market has unlocked new ways for users to engage in cross-exchange arbitrage:

The essence of arbitrage is the price differences between different markets. Currently, among the two major trading platforms supported by Boros, Binance has more large institutions and adopts an 8-hour settlement cycle, making funding rates relatively stable. In contrast, Hyperliquid has more retail users and settles every hour, allowing for faster capital flow and greater volatility in funding rates, creating more opportunities for cross-exchange arbitrage.

In addition to cross-exchange arbitrage, Boros has also launched multiple products with different expiration dates, allowing traders to engage in cross-term arbitrage: if the YU Implied APR of the earlier expiration is lower than that of the later expiration, it indicates that the market expects lower short-term rates and higher long-term rates. Traders can buy the earlier expiring YU and sell the later expiring YU, and vice versa.

**Of course, if you are not skilled in betting on the rise and fall of markets, you can also choose to become an **LP:

Boros allows users to deposit funds to become LPs through the Vaults mechanism, providing liquidity for YU trading while earning swap fees and $PENDLE rewards. Through the Boros Vaults page, we can see that the Vaults APY for BTCUSDT Binance is as high as 60.41%.

However, it is important to note that since Boros's Vaults mechanism is similar to Uniswap V2, LP positions are essentially a combination of "YU + collateral," influenced by Implied APR. Therefore, becoming an LP is also seen as a slight bullish position on YU. When Implied APR decreases, users may face the risk of high impermanent loss.

Additionally, due to the high demand for Boros, the capacity of the Vaults has become more sought after. However, as Boros transitions from a soft launch to a rapid development phase, it will gradually increase the capacity of the Vaults.

All Resources Return to Pendle: The Referral Program Initiates the Next Rapid Growth Phase

As a core product in Pendle's 2025 roadmap, Boros not only plays a key role in the Pendle ecosystem but also significantly drives Pendle's overall development through innovative mechanisms and market expansion.

Pendle's ultimate vision is to be a "comprehensive integrated yield trading gateway," and Boros not only continues Pendle's innovation in yield tokenization but also opens up the high-scale, high-volatility market of funding rates for the first time. It transforms the funding rate tokens of CEX and DEX into standardized assets (YU), expanding Pendle's ecosystem from on-chain DeFi to off-chain CeFi.

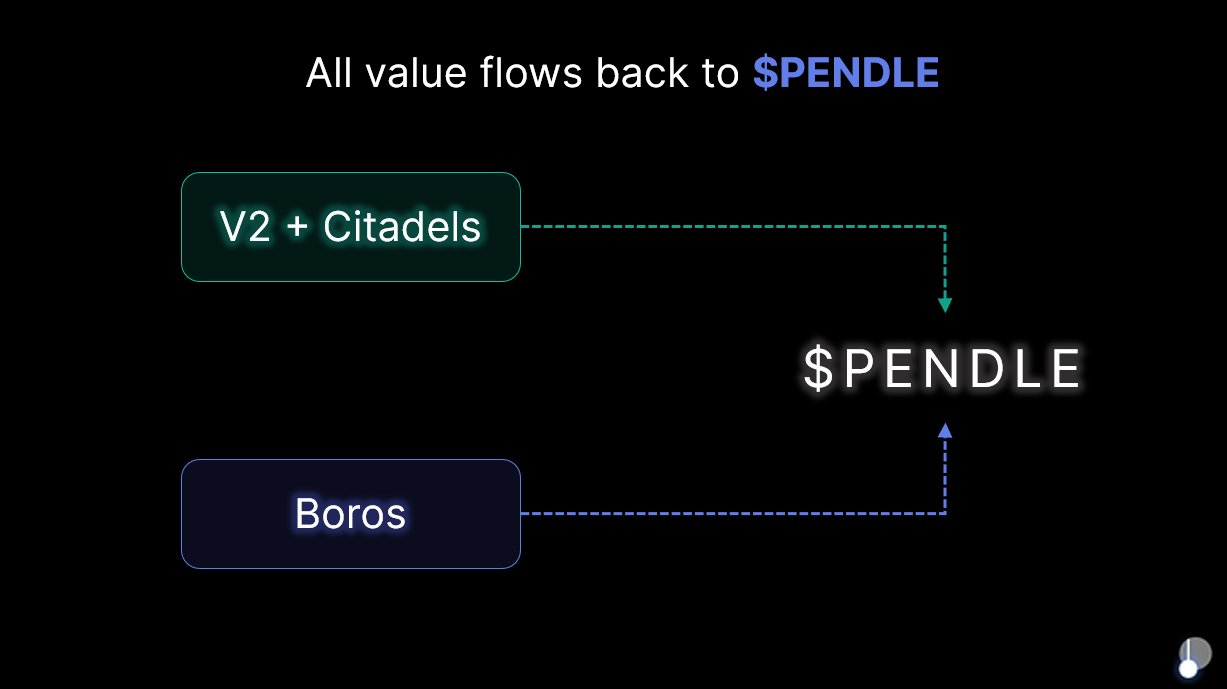

Moreover, when Boros announced the launch of version 1.0, it clearly stated that no new tokens would be issued after Boros went live, and the income generated by the protocol would continuously flow back to $PENDLE and $vePENDLE, further ensuring that $PENDLE would be the ultimate beneficiary of all value created by Pendle V2 and Boros. Meanwhile, on August 6, 2025, shortly after Boros was released, $PENDLE surged over 40% within the week, validating the market's recognition of Boros's potential.

Innovations that truly change the game often stem from the rediscovery of "long-ignored values," and Boros's focus on funding rates reveals a long-hidden treasure behind the perpetual contract market, which is large in scale but urgently needs to be explored.

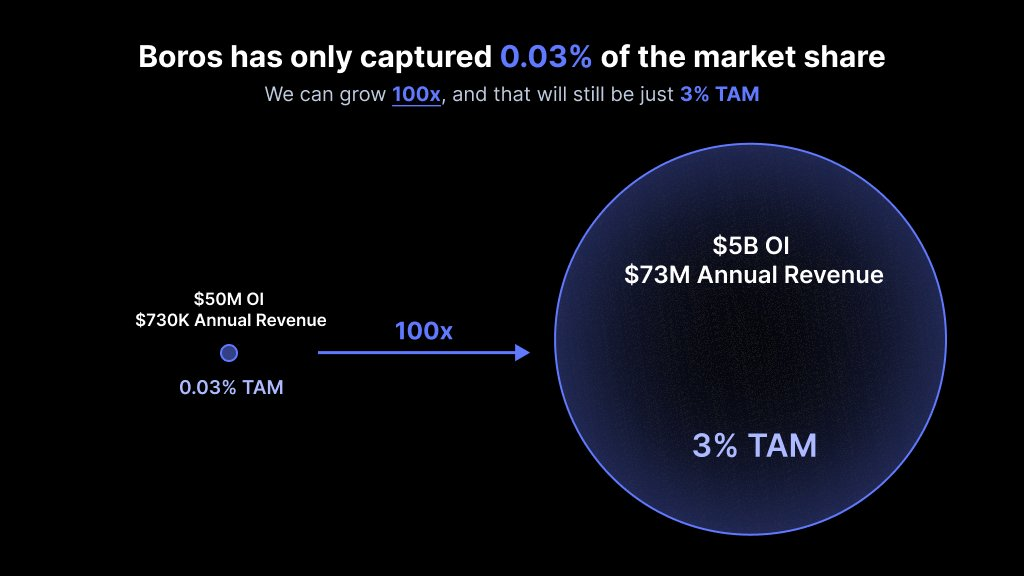

Currently, the perpetual contract market has over $200 billion in open contracts daily, with a trading volume exceeding $250 billion daily. Boros has achieved nearly $1 billion in nominal trading volume in just two months, with an annualized income exceeding $730,000. However, even so, it only accounts for 0.03% of this market.

In other words, this is a massive market with untapped potential: as the first protocol focused on funding rate trading, if Boros can continue to grow and increase its market share to 3%, it would mean a 100-fold growth opportunity.

In light of the enormous growth potential exhibited by this trillion-dollar sector, Boros has already launched several core initiatives to welcome future growth.

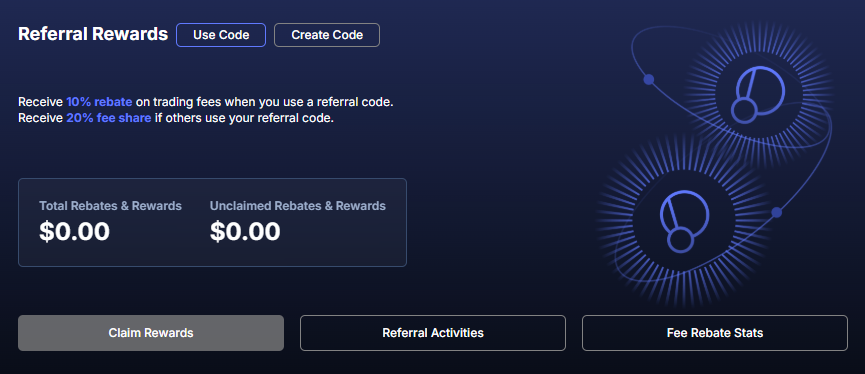

On one hand, after more than a month of refinement, testing, and observing trader usage, Boros officially launched Boros 1.0 and announced the initiation of the referral program, marking Boros's transition from the soft launch phase to a full development phase. After the referral program is launched, new addresses with nominal trading volumes exceeding $100,000 can obtain referral codes. Referrers will receive 20% of the settlement fees generated by referred users and 20% of the trading fees, while referred users will enjoy a 10% discount on trading fees.

Each referral code is valid for one year, and if the nominal trading volume exceeds $1 billion during this period, the 10% discount will no longer apply.

On the other hand, Boros will continuously optimize and improve its functions and products, and in the future, it will support more assets, more trading platforms, and higher leverage efficiency: Currently, Boros supports BTC and ETH, and will gradually include more assets such as SOL and BNB; currently, Boros supports Binance and Hyperliquid, and will expand to support more trading platforms like Bybit and OKX; additionally, as the market matures, it will support higher leverage to attract more users to leverage higher returns at lower costs. Other additional measures include increasing OI limits and vault capacities.

Beyond product optimization, it is also worth noting Boros's scalable framework:

**In addition to funding rates, Boros's architectural design can support any form of yield, including yields from *DeFi* protocols, TradFi, as well as yields from bonds, stocks, and other RWAs.** This also means that after completing the absorption of the massive funding rate market, Boros will have the opportunity to expand into more dimensions in DeFi, CeFi, and TradFi.

This further aligns with Pendle's mission of "wherever there is yield, there is Pendle." As Pendle's flagship product launched in 2025, in the foreseeable future, Pendle will use Boros as a medium to further cover the crypto finance and traditional finance markets, in conjunction with the in-depth advancement of the Citadels compliance PT plan, rapidly moving towards the vision of a "comprehensive integrated yield trading gateway."

Standing at the starting point of this absorption of all yield sources, as Boros continues to develop, we are witnessing the formation of a super yield platform that covers all types of yields and serves all user groups.

Disclaimer: This article represents only the personal views of the author and does not represent the position and views of this platform. This article is for information sharing only and does not constitute any investment advice to anyone. Any disputes between users and authors are unrelated to this platform. If the articles or images on the webpage involve infringement, please provide relevant proof of rights and identity documents and send an email to support@aicoin.com. The relevant staff of this platform will conduct an investigation.