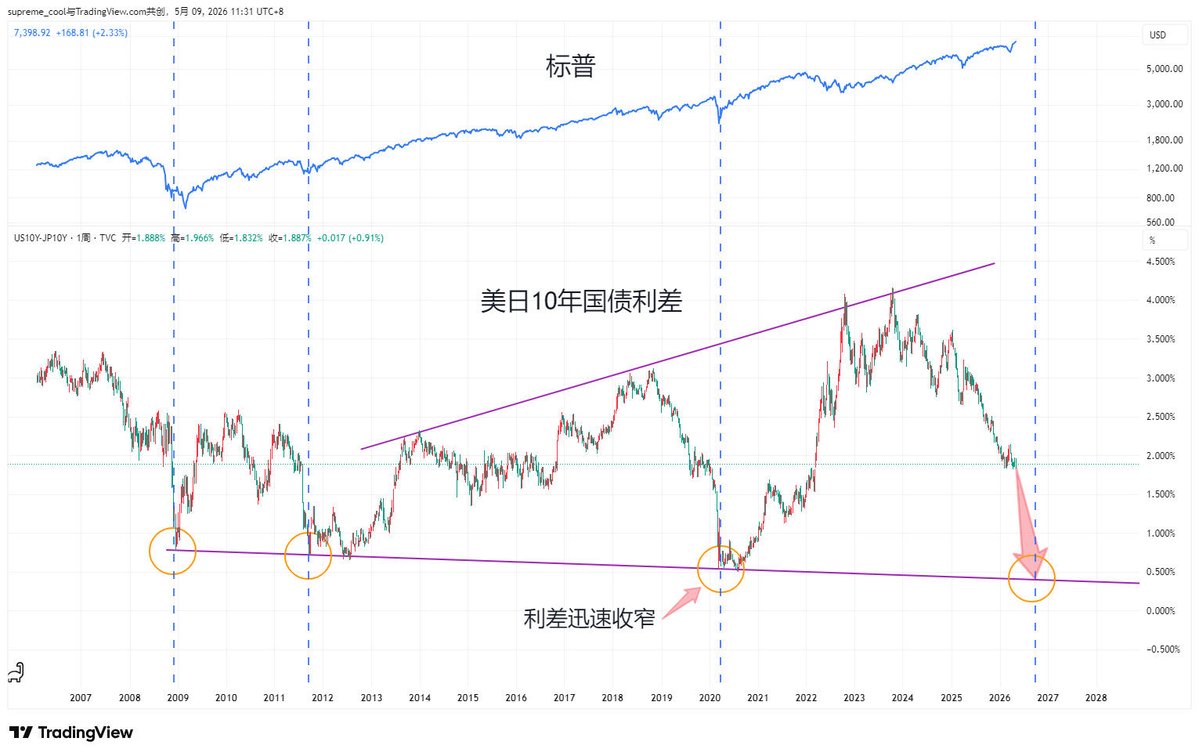

Looking at the current stage from the perspective of the US-Japan interest rate differential. Whenever this differential enters a downward trend, it usually accelerates at the end, with the gap narrowing rapidly. Historically, the US-Japan interest rate differential has hit the lower bound multiple times, each corresponding to a significant market correction. The principle is simple: when the US-Japan interest rate differential narrows quickly, a large amount of yen involved in carry trades triggers closing orders. Yen flows out of the US, leading to a sharp contraction in liquidity. As of May this year, the scale of yen carry trades has hit a new historical high, reaching $3-5 trillion, which is 2-3 times the size in 2020. If these funds are closed out collectively, the market impact would far exceed that of 2020 and 2008. From the chart, this process is already very close.