Loading...

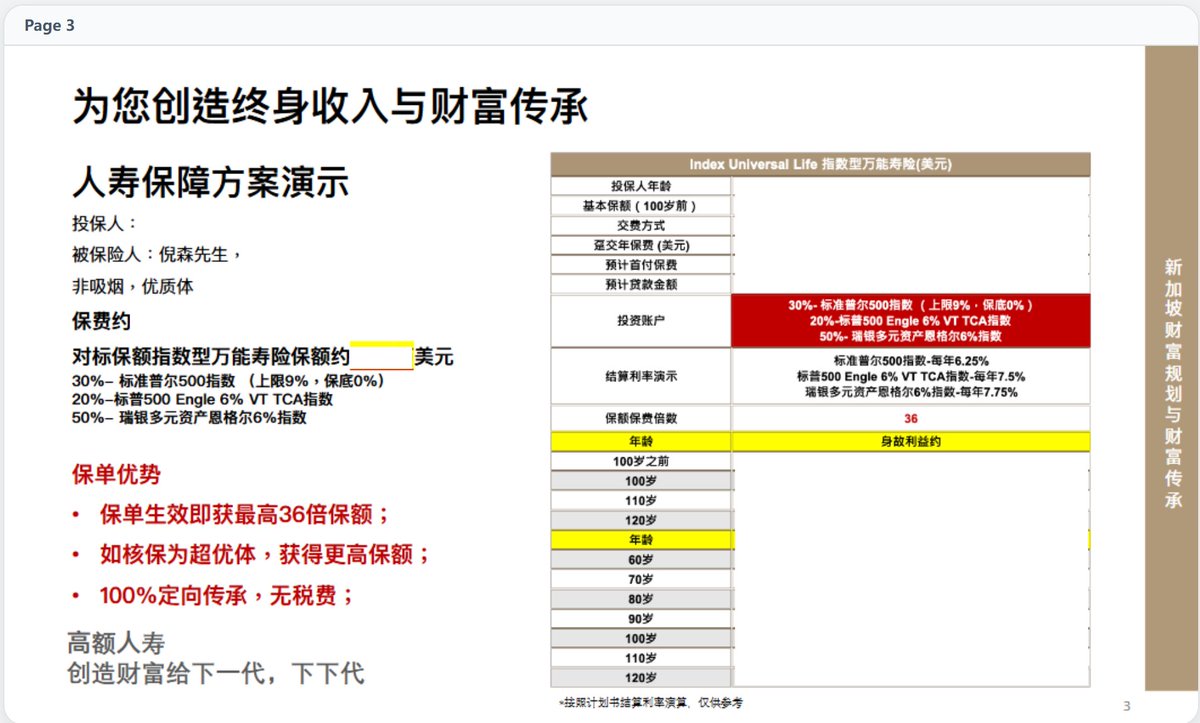

My perspective is different from Bird Bro's. I just bought a large life insurance policy, and the beneficiary is my son. The payout condition is my death. The main reason is that this is a 10x leverage insurance. The idea is simple: take a portion of my funds and calculate the payout at 10 times that amount. When I pass away, my son, Chipmunk, will receive what is equivalent to 100% of my current assets, even if I only put in one-tenth of my assets. Essentially, it doubles my net worth. Of course, while I’m alive, I can continue earning money. I’ll just consider the portion I put into the insurance as gone. If I live long enough, Chipmunk won’t have to worry about the second half of his life. If something unexpected happens to me, it ensures that Chipmunk and my family can maintain at least the same standard of living as now. That’s why I went for a health check-up recently. Surprisingly, my health is better than I expected—better than most people my age. So, while I still have some money, I decided to buy a sufficiently large insurance policy. Especially since life insurance is tax-free, and these large policies come with many other benefits, like installment payments, the ability to use it as collateral for loans, and no worries about the company running off or going bankrupt. I still believe in planning ahead. As long as I have enough money to live on while I’m alive, I want to pass on as much wealth as possible. The hardships we’ve endured, I hope the next generation can endure less of. Also, all my Bitcoin is Chipmunk’s too—I hope he can pass it on to the next generation as well.