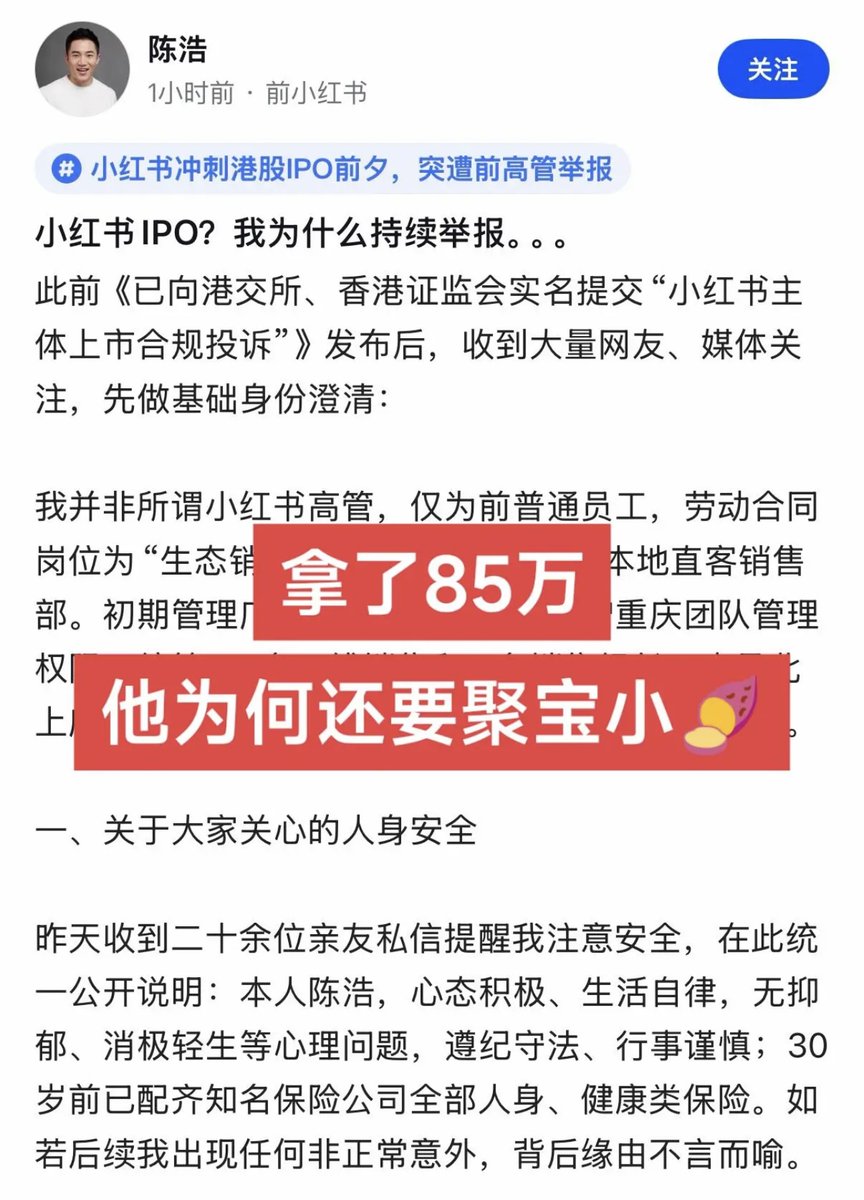

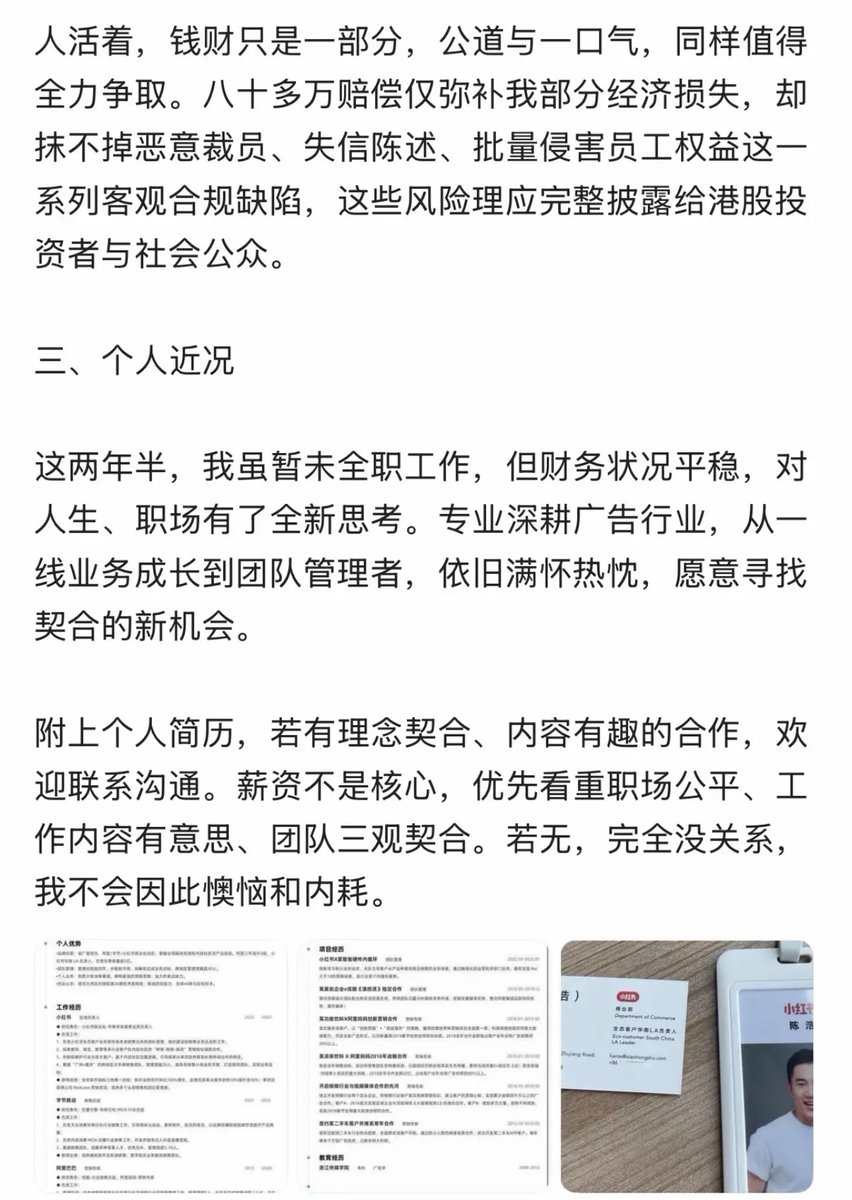

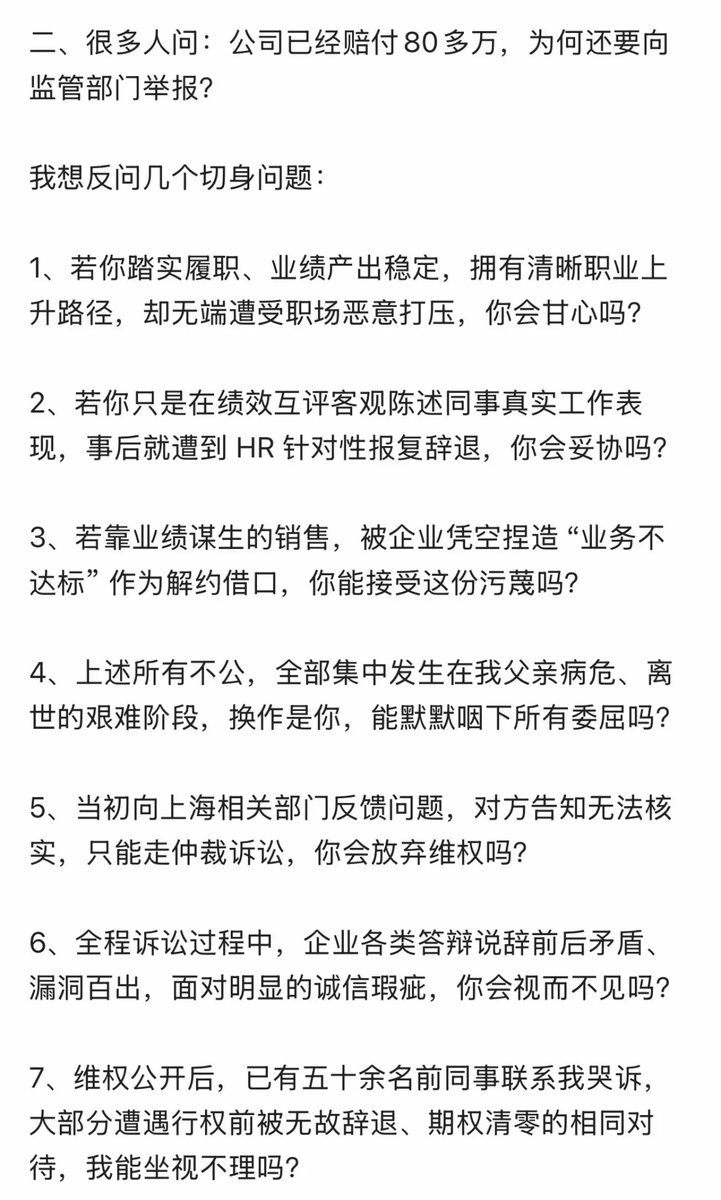

Xiaohongshu rushed to the key window of Hong Kong stock IPO and valuation, heading towards billions of dollars, but was actually reported by a former sales executive with real names! In order to forfeit 30000 employee stock options, the company fired them and insisted that the domestic entity and the overseas sweet potato were two separate companies. Now that boomerang has arrived, if you don't admit it's a company, how can you go public in Hong Kong? Xiaohongshu, which is currently in a critical preparation period for its initial public offering (IPO) in the Hong Kong stock market, has been reported by former employee Chen Hao to the Listing Department of the Hong Kong Stock Exchange and the Securities and Futures Commission. Goldman Sachs and underwriters such as CICC are participating in its IPO guidance work, and the market expects the valuation of Xiaohongshu to be between $30 billion and $70 billion. At this time, the core appeal of the real name report is not the traditional labor compensation dispute, but the major information disclosure compliance loopholes of Internet companies under the structure of variable interest entities (VIEs). Chen Hao joined Xiaohongshu in 2022 as the head of commercial direct sales in South China. When he joined, he signed labor contracts with the domestic operating entity "Shu Yi Shu Er Culture Media" and signed an employee option agreement with the overseas entity "Xingin International Holding" (commonly known as "Little Sweet Potato") for 30000 shares, which will be owned over four years. In December 2023, about 5 months before the first batch of options were about to be vested, Xiaohongshu terminated his employment contract on the grounds of "incompetence", resulting in the direct invalidation of his unclaimed overseas options. Chen Hao immediately rejected the initial compensation plan of 110000 yuan and filed labor arbitration, illegal termination of labor relationship lawsuit, and option loss lawsuit with domestic courts. In the subsequent court proceedings, Xiaohongshu's domestic legal team adopted a business strategy of defending through legal entity segmentation. The company advocates that the subject of issuing options is the overseas "Little Sweet Potato" entity, not the domestic "Potato One Potato Two" entity that signed the labor contract. This common legal isolation action in VIE architecture attempts to strip the joint and several liability of overseas listed entities in domestic litigation. However, this strategy has created a reverse business contrast when facing IPO reviews. After winning the two trials and receiving a total of approximately 850000 yuan in court judgment compensation, Chen Hao submitted the complete evidence chain including the aforementioned defense materials and court judgment to the Hong Kong regulatory authorities. This move directly hits the information disclosure bottleneck of Xiaohongshu's VIE architecture. In the compliance review of the proposed listing entity, the proposed listing company must prove to the exchange that there is a stable, legal, and unified agreement control relationship between the domestic and foreign controlling entities. However, Xiaohongshu previously made a public defense statement in domestic courts stating that "the two companies are not related" in order to avoid hundreds of thousands of yuan in option loss compensation, which directly conflicts with the "single control overall" narrative required in the prospectus. If the Listing Department of the Hong Kong Stock Exchange determines that the report involves false disclosure of substantive information, Xiaohongshu will face the cost of suspending the hearing, being forced to update the prospectus, and accepting multiple rounds of compliance inquiries. In the current strict capital raising environment, the extension of the review cycle will directly lead to the missed listing window and cause substantial drag on the early participation of venture capital capital in cash withdrawals.